Ark Invest CEO Cathie Wood on everything from deflation to Elon Musk

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Cathie Wood’s favourite scripture is Psalm 91, the hymn of protection. The founder of Ark Invest starts telling me the story of the Miracle of Dunkirk, when Allied soldiers were rescued from doomed French beaches in 1940. “A group of soldiers were huddled saying Psalm 91,” she says, “and they were one of the few groups of soldiers saved on that day.”

Wood’s eight-year-old investment management firm is named after the Ark of the Covenant – the chest said to have held the Ten Commandments – which was taken by the Israelites into battle. “Ark also has to do with battle,” Wood continues. “Battling the traditional world order is what we’re doing.”

In less than a decade, Wood has emerged as the public face of a tech-driven bull market on steroids. She championed actively managed exchange-traded funds (ETFs), a type of investment that combines the stock-picking normally associated with mutual funds with the convenience and tax benefits of ETFs.

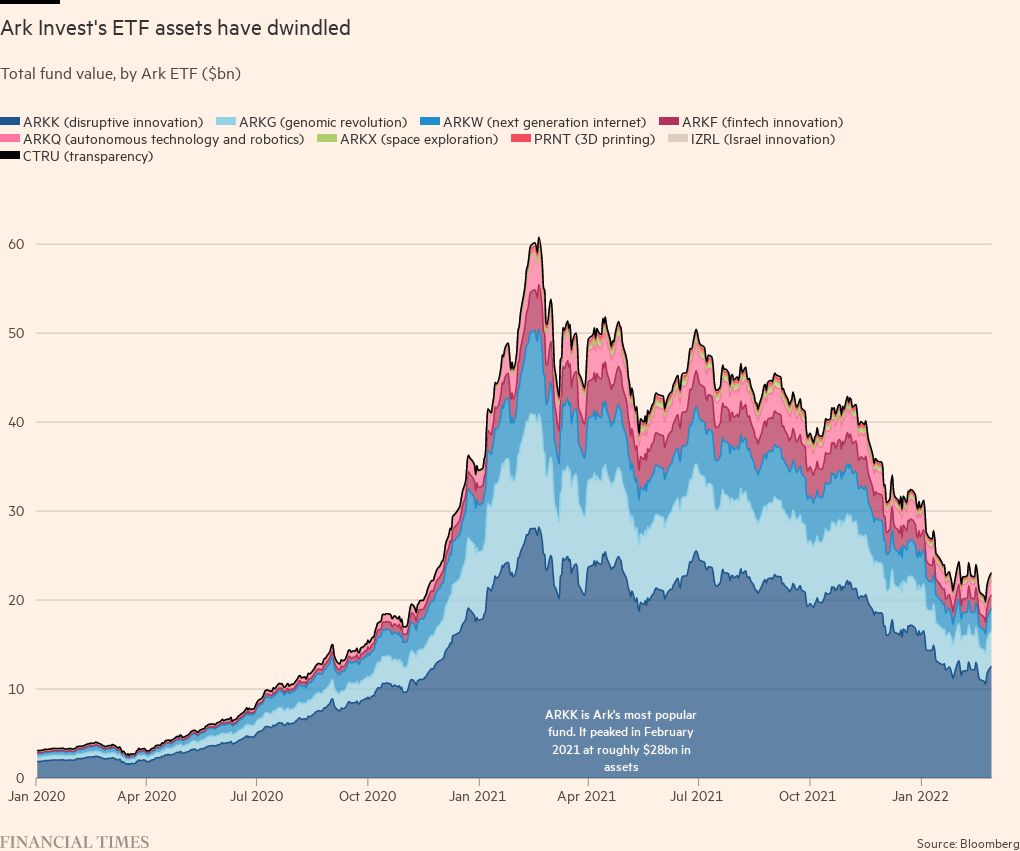

Her big, concentrated bets on “disruptive innovation”, borderline outlandish predictions on everything from shares in electric carmaker Tesla to the price of bitcoin and her savvy use of social media helped to drive assets in Ark’s overall stable of ETFs to a value of $61bn at their peak in February last year, making her the most prominent and scrutinised female investor in the world.

Ark rose during a period characterised by retail trading, meme stocks and surging cryptocurrencies, with thousands of punters opening new brokerage accounts online and using Twitter and Reddit to exchange investing ideas. By freely sharing Ark’s research, Wood developed a cult following online, where to her disciples she is “Auntie Cathie” or “Cathie Bae” and where she has spawned a range of merchandise, including a T-shirt that depicts her riding a bull with the slogan “The Queen of the bull market”. Another just reads “In Cathie We Trust”.

Wood has fans at the highest level of finance as well. “Regardless of performance trends, it’s clear that Cathie is disrupting the asset management industry in order to capture the imagination of a new generation of investors,” says Katie Koch, a partner at Goldman Sachs Asset Management. “She has demonstrated great respect for the retail investor by democratising access to information.” A top investor in growth companies tells me, “I admire Cathie’s spirit and willingness to put her head above the parapet.”

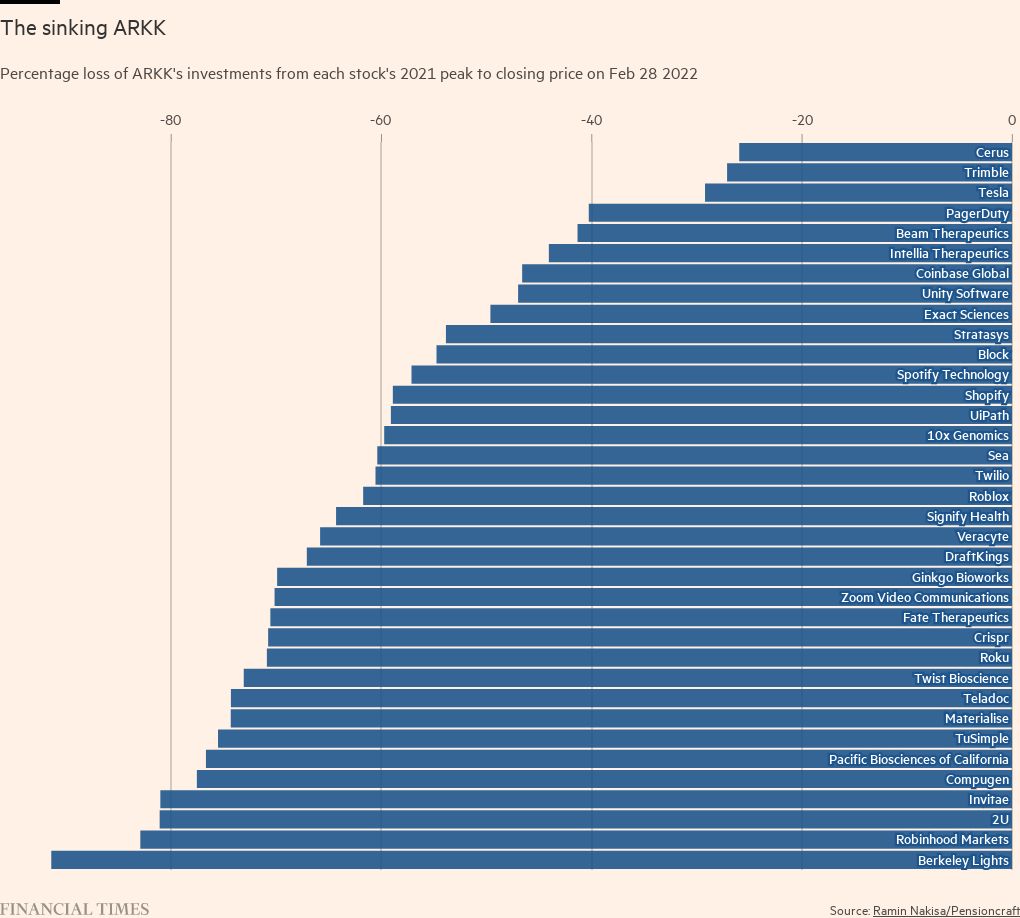

At the moment, though, Wood is in the toughest battle of her career. The 66-year-old is fighting against market momentum and trying to halt huge losses and outflows. Assets in Ark’s overall stable of thematic exchange-traded funds have dropped to $23.1bn since its 2021 high. Its flagship Ark Disruptive Innovation ETF, stock market ticker ARKK, has more than halved in value in the same period, during which time every single one of the fund’s 36 stocks has dropped. During the same period, the Nasdaq fell about 2.4 per cent.

On the face of it, ARKK boasts a stellar long-term track record: it has made an average of 38 per cent a year over the past five years, boosted by eye-watering gains of 157 per cent in 2020 as the pandemic turbocharged investor excitement about the technologies that underpin its portfolios – DNA sequencing, robotics, energy storage, artificial intelligence and the blockchain. Ark’s returns “sit in very rarefied air”, says Ben Johnson, director of global ETF research at data provider Morningstar. But most of its longer-term returns came when it had a much smaller asset base, meaning that “most investors in Ark’s funds are underwater”.

Critics – and there are a lot of them – argue that Wood’s success owes more to the Federal Reserve’s loose monetary policy than to her investment research or stock-picking prowess. Her quasi-prophetic certainty about the future is detached from reality, they argue, and Ark’s performance has been inflated by pouring money into thinly traded stocks.

“She’s brought a lot of attention to the concept of innovation, which is great,” says a prominent venture capitalist. “But the difficulty she has is that she believes in stories. Sometimes you have to disassociate the story from the business model and the valuation.” A top executive at a multitrillion-dollar asset manager says: “She tells a whole story that’s almost impervious to facts.” And a New York-based hedge fund manager adds: “She may be right in the long run, we just don’t know who the survivors will be in all of these industries. And the valuations are crazy.”

Since the beginning of this year, sentiment has been turning against the more speculative part of the market in which Ark operates, and the Russia-Ukraine war has further roiled global markets. Waves of monetary stimulus during the pandemic helped gloss over the risks of investing in the types of hot, fast-growing and loss-making tech companies Wood favours.

Now the Fed has begun scaling back support and US interest rates are likely to rise. Tech stocks, whose high prices are predicated on the potential for bumper future earnings, are seen as especially susceptible. “Every bull market has its geniuses who buy the hottest, most aggressive stocks and go up more than the market,” says a short seller who is on the opposite side of many of Wood’s trades. “But the downside of this stuff is just as spectacular as the upside. We saw this in the dotcom era.”

Many investors see parallels with the late-1990s in today’s growth-over-profits mentality and perceived invincibility of tech companies. Back then, the internet boom was followed by the stock market crash of 2000, and the subsequent downturn wiped almost four-fifths off the value of the technology-heavy Nasdaq index.

The bust made cautionary tales of fund managers such as Garrett Van Wagoner and Alberto Vilar, once hailed for their golden touch. “Cathie’s a boom or bust investor because she doesn’t disinvest or risk manage,” says Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management and Wood’s former boss at asset manager AllianceBernstein. “This is the challenge that she has had for her entire career.”

None of which seems to have dampened Wood’s conviction. “We’re at our best when the odds are against us,” she says. “For compliance reasons, I’ve been asked not to give numbers, but the compound annual rate of return expectation that we have during the next five years is the largest I have ever seen in my career.” When critics say she is nothing more than a product of the zeitgeist, Wood responds that her whole career has been about learning to ignore what’s current. And that though her thesis is simple – the future of investing is investing in the future – she’s spent a lifetime coming to it.

On November 25, I board a plane heading for Nashville, Tennessee, for an audience with Arthur Laffer, the sprightly octogenarian economist who claims credit for President Ronald Reagan’s 1981 tax cuts. A few hours later, my taxi pulls up to a pink Spanish colonial house in a leafy suburb. Laffer answers the door himself, but I barely have a chance to shake his hand before four dogs of varying sizes come bounding towards me.

Laffer is best known for popularising the Laffer Curve, which he is said to have drawn on a napkin for Donald Rumsfeld and Dick Cheney in 1974 when they worked in the Ford administration, to illustrate his argument that lower rates would boost tax revenues. My motivation for seeking him out is his decades-long mentorship of Wood. When ARKK listed on the New York Stock Exchange in October 2014, Laffer was there with her to ring the bell. Wood was one of the people Laffer invited to accompany him to the Oval Office when Donald Trump awarded him with the Presidential Medal of Freedom three years ago. (Wood supported Trump for president and donated to his campaign.)

Laffer is warm and welcoming as he ushers me past the dining room, where a long table is laid for Thanksgiving dinner, and into the kitchen. He prepares mugs of tea and plates of sushi, before leading me into the sitting room. Which is how I find myself sinking into a large leather armchair while I receive a whistle-stop tour of supply-side economics from a man who has made studying taxation and incentives his life’s work.

Framed photographs of assorted Kennedys, Thatchers, Reagans and Laffers look down upon me, surrounded by the four dogs (two Cane Corsos, a Great Dane and a Peek-A-Pom – that’s a Pekingese Pomeranian), who are now asleep. Several times, we are interrupted by calls from one of Laffer’s six children and 13 grandchildren. “Happy Turkey Day to you, my darling. I’m just sitting here with a reporter from the Financial Times. Can I call you back?”

About an hour in, as Laffer is praising Tennessee’s low-tax regime, which has lured companies such as AllianceBernstein, the mention of Wood’s former employer provides a natural segue. Laffer tells me about their first encounter in 1976 at the University of Southern California, when Wood was a student and he was a professor of business economics. Despite being an undergraduate, she lobbied him to let her into his graduate-level economics class until Laffer relented.

Wood got off to a rough start. “At the midterm, she did very poorly,” Laffer recalls. He says it was common at the time for students to cry in his class or drop out altogether as a consequence of its difficulty. “She didn’t do that. She said, ‘So what do I have to do to get better?’ And she did get better. Cathie works harder than anyone I know. She always has.”

Laffer often started his classes with a joke or some bit of relatable news to draw students in. By the time a seminar ended, the blackboard was a scrawl of equations and calculations. “We didn’t know what hit us,” Wood says. She calls Laffer’s ability to combine storytelling and hard data “a gift”.

Cathie Duddy was born in Los Angeles, the eldest of four children. Her parents were Irish immigrants who had come separately to the US “with great dreams of making it” and met at a dance in New Jersey. She credits her father, a radar systems engineer, first in the Irish Army and then the United States Air Force, with encouraging an interest in technology and economics. “It was the dawn of the electronic age, as he used to tell me quite frequently, and he was passionate about that,” says Wood. “It was also his ticket to a good life.” She describes her mother as “the laughter in our lives”.

Before Wood graduated from USC, Laffer introduced her to Los Angeles-based asset manager Capital Group. She worked at Capital for three years as an assistant economist before moving to New York in 1980 to join asset manager Jennison Associates, where she was hired as its chief economist. She was 24. “Cathie turned out to be better and smarter than all the famous economists of that time,” says Spiros “Sig” Segalas, a former US Navy officer and Jennison’s co-founder and chief investment officer. “I’ve never met anyone with as much conviction.”

At the time Wood joined Jennison, the US was experiencing severe inflation and interest rates were in the double digits. “She believed very strongly in deflation…and she was right,” says Segalas, who became another mentor. He knew many tech industry pioneers, including HP’s founders Bill Hewlett and David Packard and Intel co-founder Gordon Moore.

“Sig knew – talk about the dawn of the electronic age – he knew the people that made that happen,” says Wood. “He imbued me with the notion that technology solves problems and innovation is key to growth, that you can’t just look at earnings. You have to look at revenues. Revenue growth consistently over time means companies have to innovate, or else someone will steal a march from them.”

Around 1982, Wood wanted to resign to work for Laffer. “Do you really want to be Art Laffer’s disciple for the rest of your career?” Segalas quipped and talked her into staying. By this point, Wood was looking to move from economics into equity research and money management. Segalas had no problem with this in theory, but he was loath to take stocks away from analysts who were already covering them. So Wood waited around for what she called “fall through the cracks” companies that didn’t fit into neat categories and that other analysts didn’t want to cover.

Reuters, the database publishing company, was one example. Technology analysts felt it was a publishing company, and publishing analysts felt it was a tech company. Wood volunteered to cover it, and what was then called database publishing turned out to be the precursor to the internet. She says the experience taught her to investigate areas that others have dismissed.

She worked at Jennison for almost two decades, during which she married Robert Remington Wood and they had three children. Wood speaks fondly of this period of her career, of learning to “put the pieces of the puzzle together about how the world is going to work, not how it has worked”. She also learnt the value of diversity. “Sig has given so many women in our business their big breaks,” she says. “He really believes what a lot of women’s groups are saying and studies have shown that when you add diversity, you get better investment results.”

In 1995, Wood and her husband moved from New York to Connecticut. Robert, who had studied English literature and worked stints in institutional sales in the financial services industry, wanted to concentrate on his writing. “I said… if we move out to the hinterlands, to this wonderful place to raise children, one of us has to stay at home,” Wood recalls, “and I’m not going to be the one. So that’s what we did.” Two of his plays were produced off Broadway, including The Bridge in Scarsdale in 2002. The couple eventually divorced in 2003, and Robert died of cancer in 2018. Before he did, Wood welcomed him back into the house so the family could be together.

In 1998, as the dotcom bubble was reaching its climax, Wood and one of her colleagues, Lulu Wang, left Jennison to set up a fund in New York called Tupelo Capital Management. By the end of March 2000, the peak of the tech bubble, Tupelo’s assets under management had reached almost $1.4bn, according to a regulatory filing. Twelve months later, Tupelo’s assets had slumped to around $200mn, according to a separate regulatory filing.

In other words, Tupelo’s assets under management lost over four-fifths of their value during the dotcom crash. It’s not possible to establish how much of this was due to performance losses and how much to investors pulling their cash. Wood says, “While we disagreed about strategic moves at the end of my tenure, we parted ways with mutual respect.” Wang declined to comment.

Wood dusted herself off and joined AllianceBernstein later that year as chief investment officer for thematic portfolios. Lisa Shalett, her boss at the time, recalls her “first memory of Cathie is of a whirling dervish running around in a trench coat weighed down by bags and bags of research. You would see her early in the morning or running from the office late at night to catch the train.”

But Wood’s track record at AllianceBernstein was both volatile and underwhelming, according to Morningstar. Shalett says that Wood’s investing style was a “rollercoaster ride” for clients and that it found greater traction with retail investors than with the institutional market. Even so, Wood continued to display the same conviction Segalas had admired at Jennison. “She is disciplined and missionary in her approach. She’s an evangelist for tech, and it’s infectious,” says Shalett. “We all love a great story. She does her research; she believes what she believes. Sometimes when the market moves against her, she digs in more.”

On a glorious August day in 2012, Wood returned home from work to an uncharacteristically quiet house. Her three children were at summer camp, and it was the first time she’d been alone that long since she moved to Connecticut in the mid-1990s. “I’m kind of stunned by the silence,” Wood recounts. “I walk into the kitchen to the counter. And I’m not happy, and I’m not sad. I’m just in that zen state.

“Boom. That’s when it hit me. Why don’t you apply the technologies that have been disrupting other industries to your own? Think about it: your industry finances all of these disruptions that have changed other industries, and it hasn’t embraced them itself.” Within five minutes, the key foundations of what would become Ark’s approach came to her: adopting open source research, embracing online media, investing in innovation.

Wood tells me the epiphany marked the culmination of six years of prayer. From about 2006, she had struggled to make sense of the changing financial landscape. On the advice of someone at her church, Walnut Hill Community Church, Wood had spent each morning reading from a devotional as her coffee was brewing, asking God to “show me what to do”. When it all came together, she knew “I had to start this firm, and I knew it would be successful. I knew it would be difficult too.”

Wood believes she was “born with the gift of faith”, and it deepened through testing times like the stock market crashes in 2000 and 2008 and her divorce, she told an interviewer in 2020 on Jesus Calling, a podcast. When we discuss her religious practices, Wood chooses her words carefully. “Before I make a big move, I will always pray,” she says. “Prayer is a form of meditation too. It’s a very grounding experience. People who meditate deeply experience the same thing I do. And in those moments, I get answers… The holy spirit, if you want to just dwell on that, is the same thing as the Force.”

Initially, Wood approached Peter Kraus, then chair and chief executive of AllianceBernstein, with her unorthodox pitch: she wanted to launch an actively managed ETF business devoted to disruptive and innovative companies. At the time, the ETF industry was dominated by passive funds that tracked an index such as the S&P 500 and was run by players like BlackRock, Vanguard Group and State Street Global Advisors. “I said no,” Kraus, who is now chair and chief executive of asset manager Aperture Investors, tells me, “because it didn’t seem like a high probability it would succeed. It was not because I didn’t like her. I don’t regret it.”

Laffer also had doubts. “I talked with her at enormous length when she was going to set up Ark,” he says. “She weighed my advice and then went the other way.” Laffer worried about Wood giving up a stable job to start up in a fledgling part of the market and putting too much of her own money into Ark. “I did not want her to lose everything she had.”

In January 2014, Wood founded Ark. For the first three years, she funded the business with her own money. (She rewarded Laffer with a small stake in Ark Invest, of less than 1 per cent.) Wood received an early investment of around $20mn for her first four ETFs from former hedge fund manager Bill Hwang, whom she met when they were both advisers to a religious group that ministers to young people on Wall Street. Hwang is now infamous for the implosion in March 2021 of his family office, Archegos Capital Management. A person with knowledge of the matter says Hwang admired Wood’s expertise in growth stocks, but that the investment in Ark was a show of support, rather than strategic. Hwang declined to comment for this article.

For its first two years, Ark built but the clients failed to come. So Wood sold minority stakes and signed deals to help sell her funds. First to Resolute Investment Managers, an asset management platform and distributor, in 2016 and, the following year, to Japan’s Nikko Asset Management. It would take the pandemic – and a big and prescient bet on Tesla – to turn Wood into a star.

In October 2020, as Ark’s performance was riding high, Resolute said it intended to exercise an option to buy a majority stake in the company. Wood pushed back. One former Ark employee tells me that, during this period, Wood was convinced she would regain control of the company even when colleagues thought it was highly unlikely. Wood turned to Todd Boehly, founder of Eldridge Industries, a holding company that makes investments, to lend Ark the funds to repurchase Resolute’s option and later reward Ark’s top employees with a share of the business.

The former employee says Wood “feels very much on a journey doing God’s work. She’s moved by forces beyond the asset management game. She has confidence from her craft, but also she feels like she’s on the right side of… I don’t know what to call it. It gives her energy and strength. The God element is more a guide of her life path. God is not telling her to buy or sell shares.”

Under the terms of the 2020 deal, Resolute remained Ark’s main distribution partner in the US, and Wood remained its majority shareholder. She was more personally exposed than ever. Resolute sold at what would turn out to be the top of the market. And when 2021 arrived, Ark’s performance began to unravel.

The town of Bethel is named after a Hebrew word meaning “house of God”. Unlike Connecticut’s Gold Coast, where prominent financiers like hedge fund manager Ray Dalio own expensive waterfront properties overlooking the Long Island Sound, the sleepy inland streets here are lined with traditional New England timber-framed saltbox houses. Many of them are flying the Stars and Stripes. I’m here to attend a morning service at Walnut Hill, where Wood was an active member of the congregation until she moved to Florida last year.

Walnut Hill is a nondenominational, evangelical megachurch, with four campuses across the state. Its purpose is “igniting a passion for Jesus in Connecticut, New England and around the world”, according to its website. In the vast entrance hall of the Bethel Campus, a sign hangs above the door reading “Go bring heaven to earth!”

As I wait for the service to begin, I track down Reverend Brian Mowrey, one of Walnut Hill’s lead pastors. Wood has been coming here for more than a decade and has “been very engaged in life here”, Mowrey tells me. “She has a unique gift of being a futurist, very discerning of where things are going in our world, a great sensitivity to how God is moving and speaking.” He won’t say whether he’s an investor in Ark.

We make our way to the darkened auditorium for the service, picking up our own individually packaged Eucharist on the way in. The lingering pandemic also means that the hall, which has capacity for hundreds of people, is far from full. Everything is broadcast online. The service is accompanied by a live band, and today’s theme for the homily is “Developing a Heavenly Mindset”.

Afterwards, I’m standing in the church car park waiting for a friend to come and collect me, when a retired couple, John and Rita DePasquale, strike up a conversation. They have noticed me looking a bit lost. John, 76, who used to work in promotions and consumer packaging, says he came to his faith in his early thirties. “I was burning the candle at both ends, and then I found another way, a spiritual way.” He met Wood through the church but says he’s had “very little” interaction with her. He did, however, become an investor in Ark, following a recommendation from one of its clients: DePasquale’s son, Reverend Adam DePasquale, another of the lead pastors at Walnut Hill.

The elder DePasquale says that, normally, his investment criteria include being a well-known company that’s a leader in its field and paying a consistent dividend. Still, Ark piqued his interest enough that he made a roughly $12,000 investment towards the end of 2020, when ARKK was trading at around $120. “The things she’s invested in made a lot of sense,” DePasquale says. “I got a sense that she sees paradigm shifts taking place – a gift.”

Three months later, I check in with DePasquale to find out how he’s feeling about his investment, which is now down 40 per cent. He says he doesn’t have “any desire to bail out” or any financial need to sell right now. “I’ll wait. I have faith that it will come back, and she’ll turn it around. I think she has the right attitude towards innovation… I don’t want to buy high and sell low. That’s not a remedy to make money.”

As our telephone call draws to a close, DePasquale asks if I would mind if he prayed for me. Not at all, I respond, assuming he means later on, privately. “Dear God,” he starts saying into the other end of the line, “thank you for Harriet and how she has used her skills and passion to seek wisdom… May you bless and protect her.”

In February 2019, Tesla’s stock was trading at around $60. Ark, which holds a significant position in the electric carmaker, was bullish on its prospects, estimating that its share price could reach $3,000 by 2025. Wood was in a meeting room at the firm’s New York offices when she heard screams and laughter from her colleagues outside. She went out to find that Tesla chief executive Elon Musk had sent a direct Twitter message to Tasha Keeney, an Ark analyst, complimenting her on her work. Later, Musk joined Wood and Keeney on Ark’s regular FYI - For Your Innovation podcast. When I contact Musk via email about this story, he shoots back a single sentence: “Cathie and the Ark team think deeply about the future and are mostly correct. — EM”.

Ark’s ability to speak in the emoji-laden, highly referential language of the meme stock generation is one example of what Ark means when it markets itself as an “untraditional investment manager”. Another is atypical hiring. The company has fewer than 50 employees, including around 20 in research and investing. Wood has surrounded herself with a team of young analysts, with backgrounds in subjects such as computer engineering or molecular biology, rather than a traditional grounding in finance. She says this is the best way to identify disruptive trends and to avoid consensus thinking. “I really believe that young people are at an advantage,” she says, because they “have one foot in the new world” and are native to certain parts of the market such as cryptocurrencies.

Wood says the active management industry is dominated by short-term thinking and index trackers that avoid taking big bets and have high position overlap with their peers. Fear of the new, in other words. Ark set out to have a portfolio that has little overlap with the Nasdaq and the S&P 500. “The old world order describes [Ark] as highly speculative, highly risky and these other disparaging words,” she says. “Whereas what we are saying is, ‘No, you are in harm’s way. You are taking a risk by not doing the kind of research we’re doing.’”

Closely guarded proprietary research is the norm in the mainstream asset management industry. But Ark publishes all its research and stock price targets online; it also discloses its positions and trades, which one critic says amounts to “playing poker with their cards faced up”. This practice certainly makes it easy to follow Wood. Unaffiliated websites, such as Cathiesark.com, publish the positions, trades and weight of all companies in Ark’s stable of ETFs daily. An entire ecosystem of copycat and related products have sprung up around Wood’s funds as a result.

This includes products that allow investors to magnify their exposure to Ark’s ETFs – or to directly wager against them. Last November, Tuttle Capital Management unveiled the Nasdaq-listed Tuttle Short Innovation ETF (ticker: SARK), which gives investors the ability to bet against Wood’s ARKK. Since launching, SARK has grown from $5mn to $325mn in assets under management and is up 24 per cent this year. “Some people are using it as an anti-Cathie Wood bet,” says chief executive Matthew Tuttle, while others are using it as a hedge against their exposure to growth stocks at a time when interest rates and inflation are rising.

Some people see flaws in Ark’s business model. Edwin Dorsey,

a short seller and author of the Bear Cave newsletter, has criticised the team’s lack of experience. For example, Ark’s chief operating officer, Tom Staudt, who is in charge of its risk management, is a former account executive at a television station in Michigan. “At Ark you get out-of-the-box thinkers from non-traditional backgrounds,” says Dorsey. “But it relies a lot on young analysts who might be in over their skis.” He believes that Ark’s research is good at identifying technological trends, but he doesn’t “think it’s that rigorous when it comes to selecting individual stocks”.

That can mean missing red flags that ought to have come up during due diligence. Dorsey says examples among Ark’s current or previous investments include: German payments company Wirecard, which collapsed into insolvency in June last year, following a multiyear fraud exposed by the FT; and, Vuzix, an augmented reality glasses company in which Ark owns more than 10 per cent, which has a history of consistent unprofitability, a short seller lawsuit and an informal enquiry by the US Securities and Exchange Commission.

The validity of Ark’s financial models and headline-making predictions has also come into question. At least two people reckon they found erroneous judgments in the company’s publicly released valuation model for Tesla. These errors, they believe, contribute to an overestimation of what the electric carmaker could be worth. Some of Wood’s public predictions strain credulity. Notably in a 2018 video, she declared “monogenic stem cell therapy” a $2tn revenue opportunity, with “polygenic” versions of the treatment worth “however many trillions” more. Monogenic stem cell therapy is not a concept scientists recognise. Wood says Ark’s research on innovation is “the best in the financial world.”

And then there’s Ark’s footprint in the marketplace. When it buys and sells positions in smaller, less frequently traded companies typical of the innovation space, Ark can have an outsized impact on their share price because these types of positions are less liquid than blue chips like Tesla and Zoom. (Across its ETFs, Ark owns stakes of more than 5 per cent in 37 companies, and owns more than 10 per cent of 18 of these companies, according to Morningstar.)

“As Ark has been buying these small-cap companies, it has been pushing their share prices up,” says Dan Izzo, chief executive of GHCO, a registered market maker. “It’s a self-fulfilling prophecy on the way up.” Crucially, he notes, this works both ways. “If redemptions made Ark a forced seller of illiquid names then it could push down their share prices.” This could result in a downward spiral for Ark.

For all Ark’s talk of transparency, it takes more than four months before Wood finally agrees to an interview. By this point, it’s mid-February and ARKK has halved from its peak the year before. The short sellers are being vindicated. Wood pops on to my laptop screen, instantly recognisable by her trademark horn-rimmed glasses and poker straight hair. She looks smart in a striped shirt, dark highlights framing her high cheekbones and perfect white teeth. “We are as calm and focused as you could possibly imagine,” she says. Despite the market turmoil and the mounting losses in her portfolios she sleeps “very easily” at night, “knowing that we have never been in a period of more innovation in history”.

There’s one exception: the prospect of investors pulling their money from Ark’s fund at the worst possible moment. If clients do so now, Wood says they will turn “what we believe are temporary losses into permanent losses. What’s going to happen is the same thing that happened in 2008-2009. Those who got out had such seller’s remorse” because they missed the subsequent market rebound.

We take the big controversies facing Wood and Ark one at a time.

Critics have suggested that the firm’s transparency makes it vulnerable to front-running. If the market can see everything Ark is doing, traders could use that information to try to get ahead of it. This is especially a risk in a downward market. If Ark, for example, had to sell positions to meet redemptions, other investors could see that and sell off first, pushing down prices even more. Wood dismisses this. “It’s very hard to front-run us,” she says, adding that if she sees the price of a stock that Ark is buying starting to move up dramatically, she halts the order. The same thing happens on the way down. “We can stop the sale if [they’re] driving a stock down because they know we’re just going to be selling, selling, selling. I can stop it if I want to.”

Wood is more philosophical about the short sellers: “Well, that’s what makes a market. And if we’re right, they’re going to have to cover all of their shorts, and that’ll help with the swoosh when it happens. And I truly do believe it will.” She says she does not take the existence of SARK and others like it personally. “They’re not doing any research. That’s why that strategy is not going to work in the long run. It’ll work from time to time when we’re in risk-off periods.”

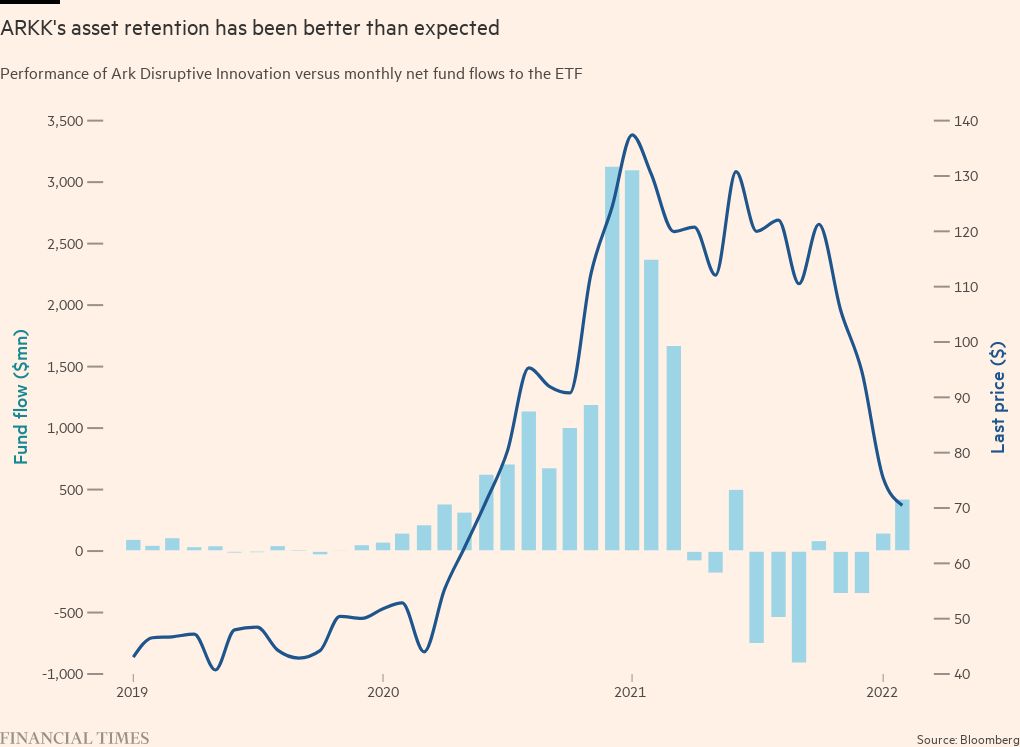

Ark allows investors to redeem their money on a daily basis; the risk in a downturn such as this one is that they pull out in droves. But Ark’s asset retention has been better than expected, says Wood. She believes this is a result of Ark’s communications strategy. “We overcommunicate. We are constantly putting out research. We are tweeting to let our clients know nothing has changed from our point of view.”

She believes that “this has helped our clients trust us” and keep their Ark investment. Tuttle agrees: “ARKK has not had as many outflows as you’d expect, given the returns.” But he thinks it’s because “retail investors have been conditioned to ‘buy the dip’ in growth stocks”, a strategy that has worked since 2009. “At some point there’s a level where everything starts to waver,” he adds, “I just don’t know where that is.”

An important element of Wood’s vision — and one of the drivers of her seemingly boundless optimism — is that the deflationary trend of recent decades and generally low interest rates will continue: technological innovation suppresses costs, while companies whose products are being rendered obsolete will have to cut prices. “Many people think we have a permanent inflation problem,” she says. “We don’t.” If anything she believes that problems that emerged during the pandemic “are accelerating the rate at which innovation is taking place”.

But Wood is fighting against the tide of central banks. Jennison’s Segalas says: “The problem right now is that interest rates are going up, and that tends to hurt valuations, particularly of growth companies with no current earnings power. A lot will depend on what happens to inflation and interest rates as to when her strategy is going to work.” He adds: “Eventually I think she’ll be right, but I don’t know how long that takes.” Eldridge’s Boehly says, “Ark has low fixed costs, very modest leverage and substantial liquidity, which allows it to ride out market volatility.”

The challenge for Wood is that she may be correct in identifying the big trends in innovation but back the wrong companies. Even if her bets are right in the long term, Ark’s losses in the short term could wipe it out. To paraphrase Keynes, the stock market can remain irrational longer than many fund managers can stay solvent.

Wood has clearly pondered the question of longevity. “Many people in our business… they’d be quite happy to see us disappear,” she says. Repeatedly during our conversation she refers to herself as a “lightning rod” for the industry. To these critics, Wood represents the worst aspects of a frothy market, the gate-crashing of low-information retail investors and the triumph of a good story over hard data. None of which can end soon enough. For her retail following, she represents a middle finger to all of that. Fans want to believe her stories of a better, brighter future filled with flying cars, green energy and longer, healthier lives.

But as the interview draws to a close, Wood is keen to make one last, important point. When it comes to Ark’s investments, “the courage of my conviction” is not the result of any higher calling. It “comes from our research”, she says. “I just want to make that very clear.”

Harriet Agnew is the FT’s asset management editor

Follow @FTMag on Twitter to find out about our latest stories first

FT Asset Management newsletter

Our weekly inside story on the movers and shakers behind a multitrillion-dollar industry. Sign up here

Comments