Why nature’s future underpins the future of business

Simply sign up to the ESG investing myFT Digest -- delivered directly to your inbox.

For anyone wanting to put a monetary value on nature, Californian farmers can offer a compelling example. They are seeing a rising incidence of bee burglary. So essential are these pollinators to farmers that the state’s beekeeping association now offers rewards of up to $10,000 for information leading to the arrest and conviction of hive thieves.

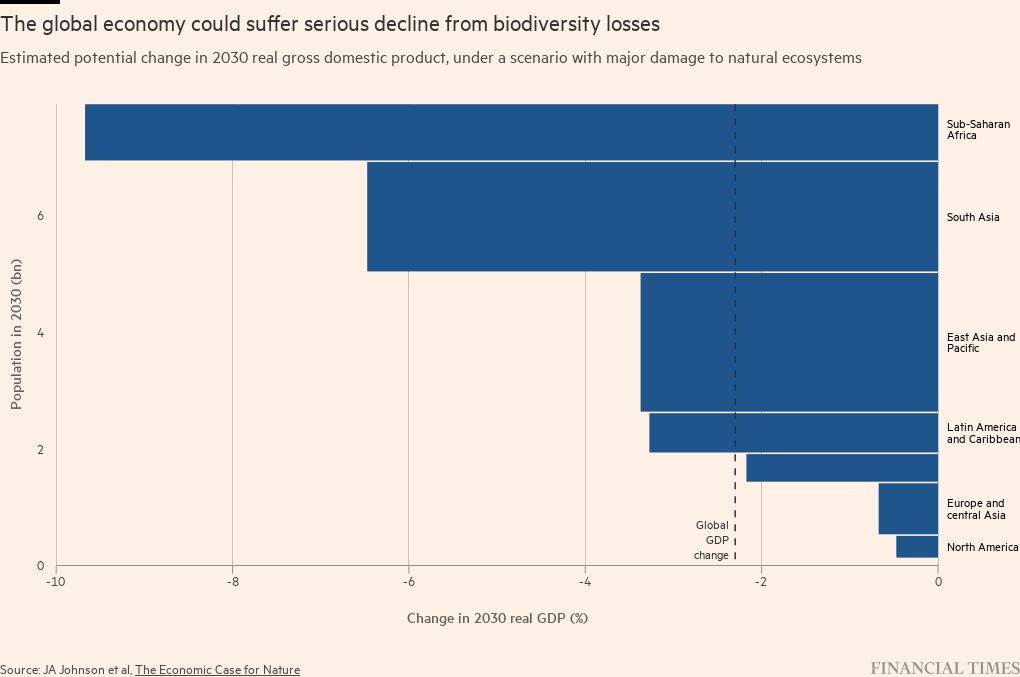

The global economy’s dependence on nature is becoming clearer. According to the US Department of Agriculture, pollinators underpin one in every three bites of food eaten on the planet, while the World Economic Forum has estimated that, through everything from water retention to carbon sequestration, $44tn of economic value (more than half global gross domestic product) is “moderately” or “highly” dependent on nature.

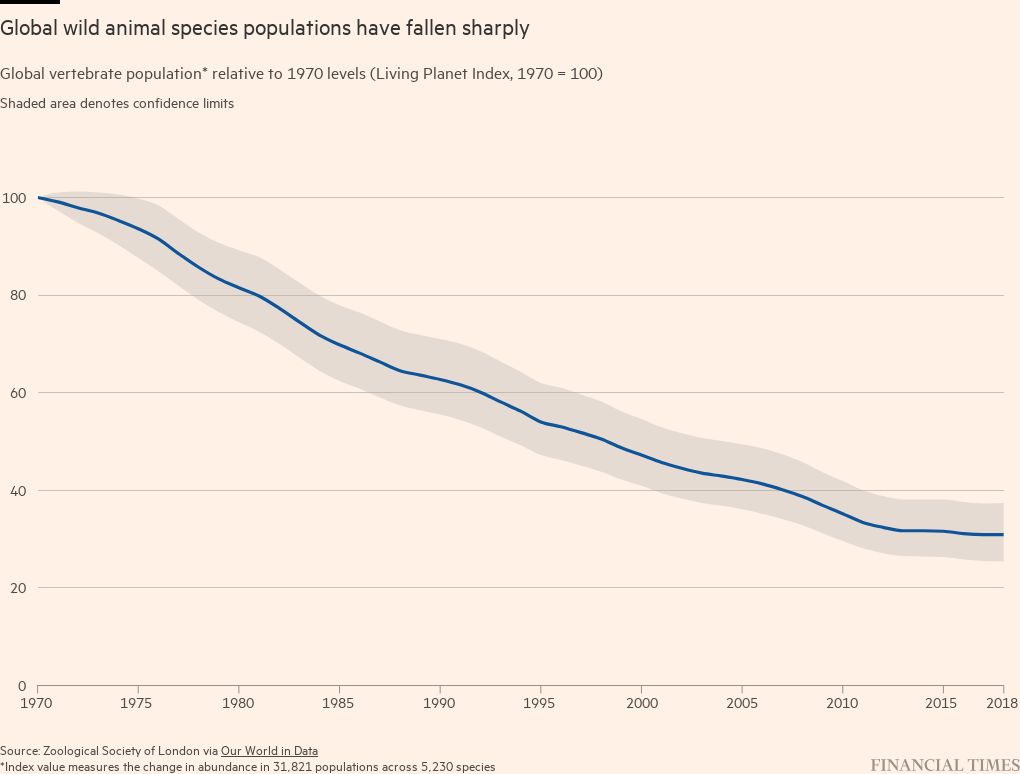

Given the accelerating rate of nature loss, the WEF’s figure is alarming. Scientists say that, unless measures are taken to slow the drivers of biodiversity loss, many of the roughly 1mn animal and plant species currently threatened by extinction will disappear within decades.

Among the dire potential consequences is the impact on efforts to tackle climate change. By taking vast amounts of carbon from the atmosphere and storing it, natural systems such as soils, forests, grasslands and oceans act as “carbon sinks” that are essential to stabilising the world’s climate.

If losses in nature (the natural world) and biodiversity (the variation in that world) pose a dire threat to humanity, they also present risks to business and finance, both through companies’ impact on natural resources and their direct or indirect dependency on them.

Companies are likely to face costlier and scarcer raw material supplies, reputational risk, pressure from campaign groups, legal challenges and tightening regulation. And investors worry that those risks could show up in their portfolios.

Moreover, because nature’s costs are not currently being accounted for, companies have a false sense of security, says Paula DiPerna, author of Pricing the Priceless. She compares it with staff costs. “If you could get away with not paying any of your workers, your books would look a lot better,” she says. “We’re getting away with not paying nature, the ultimate worker.”

Last year’s UN biodiversity summit in Montreal attracted an unprecedented level of interest by private-sector companies, who turned out in force on the sidelines. The conference ended with an agreement by governments to put 30 per cent of the planet under formal protection by 2030 — and to impose nature reporting requirements for companies.

Meanwhile, the final recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD) came out in September, giving companies a framework similar to that developed by the Task Force on Climate-related Financial Disclosures (TCFD), which galvanised corporate reporting on climate risks.

Critically, governments are drawing links between climate change and nature, with funding for nature conservation and biodiversity promotion available through green government programmes such as the US’s Inflation Reduction Act, the European Green Deal and Brazil’s National Green Growth Program.

“These are not only about climate change,” says Simon Zadek, executive director of non-profit NatureFinance. “They are where the nature agenda and the climate change agenda hit the industrial and economic strategy agenda.”

Not all FT Moral Money readers are worried. “Are there big risks?” wrote one in response to our survey. “There could be reputation risk in egregious cases. But broad public concern is just not there, and the ‘concern bandwidth’ is already taken up with climate, inequality, and other issues.”

However, most see dangers ahead. “The loss of biodiversity is a greater danger to human life than carbon emissions,” wrote one, while another argued that inaction would risk “system collapse”.

Those who agree see plenty of work ahead, from financial innovation to protecting the resources one FT Moral Money reader describes as “silent contributors to a company’s success”. And while nature’s complexity may leave some feeling overwhelmed, scientists, economists, sustainability experts and others argue that companies and investors must push nature and biodiversity up their list of strategic priorities.

“This is not a corporate social responsibility issue for business and finance,” says Tony Goldner, TNFD executive director. “It’s a central strategic risk management issue because the future cash flows of business are dependent on the flow of nature’s services.”

Accounting for nature

In 2011, the sportswear business Puma did something unusual: by imposing internal accounting measures such as a price per tonne of carbon and per cubic metre of water, it added up the cost of its use of ecosystem services. The resulting “environmental profit-and-loss” account statement was striking. Against that net earnings for 2010 of €202mn, it estimated aggregate environmental costs of some €145mn.

Mandatory environmental profit-and-loss accounting might be some way off, but the risks to business are not. “Every single company is in that situation,” says DiPerna. “People keep investing in companies based on a false sense of their investability.”

Some blame can be assigned to traditional measures of success such as gross domestic product, wrote the University of Cambridge’s Sir Partha Dasgupta in an influential 2021 review of the economics of biodiversity commissioned by the UK government. GDP, he wrote, is “wholly unsuitable” for measuring sustainable development, particularly since “eroding natural capital” is how most nations have achieved economic growth.

Links between nature and business fall into two buckets. In one are dependencies on natural resources — a drinks company’s water consumption, a pulp and paper company’s need for trees, a food company’s reliance on pollinators and so on. In the other are the effects that business activities have on those resources.

Both are equally important, argued one FT Moral Money reader, who told us: “For individual companies and investors, impacts and dependencies on biodiversity must be assessed and addressed like any other material business risk.”

In the food and beverage sector, where companies rely almost entirely on naturally produced ingredients, one of the biggest dependency risks is soil degradation. “The more that soils are degraded, the less productive and efficient they become,” says Owen Bethell, who leads environmental public affairs for Nestlé, the world’s biggest food company by sales.

For financial institutions, meanwhile, credit risks loom large. As Dasgupta highlights in his review, the degradation or collapse of ecosystems would disrupt the supply chains of many companies, denting their ability to service their debt and increasing their likelihood of default.

If dependencies on nature pose tangible threats to companies and investors, the consequences of industry’s negative impact on nature are no less worrying. These include tightening regulation, reputational damage and the increasingly loud voices of local communities in affected areas.

Zadek at NatureFinance points to a further risk: that investment portfolios contain assets linked to criminal activities such as wildlife trafficking, illegal deforestation and pollution. According to the Financial Action Task Force, such crimes generate up to $281bn annually in illicit gains.

“No financial institution wants to be accused of investing in enterprises that benefit directly from nature crimes,” he says.

In November, a legal opinion published in Australia created fresh jeopardy for board directors by concluding that they could be held personally liable for breaching diligence and duty-of-care obligations if they did not consider nature-related risks.

Threats of legal action may serve as a wake-up call for companies and investors who have often proved slow to respond to warnings on nature loss.

The language around nature is part of the problem, says DiPerna. She cites the word biodiversity, which for her conjures up something beautiful but non-essential. “It sounds like jewellery. It doesn’t sound like what it is: an engine that makes all economic activity possible.”

For the TNFD, use of terminology familiar to business and finance was important when developing its recommendations. “We took on board the approach of thinking about nature as natural capital,” says Goldner. “That provides the kind of language system for thinking about nature that is accessible to market participants.”

Another way of looking at companies’ exposure to nature and biodiversity loss is as an enterprise risk similar to cyber security, says Chris Goolgasian, Wellington Management’s climate research director.

At one point, cyber security wasn’t an enterprise risk, but it certainly is today,” he says. “Why is this any different? Once you realise how material it is to a company’s operations, then you’d say it’s an enterprise risk — we probably need a board expert on it, and we need to fund it.”

New financial tools

In the race to tackle threats to nature, financial innovation is being used to harness capital for the protection of ecosystems while delivering returns for investors. Piloted in Tahoe National Forest, California, the Forest Resilience Bond pays for the removal of the undergrowth and shrubs that act as tinder for wildfires.

To develop the bond, non-profit Blue Forest designed a structure similar to a pay-for-success contract. Investors, including Calvert Impact Capital and the Rockefeller Foundation, provided $4mn in upfront capital to pay for forest management services across 15,000 acres of national forest.

“The priceless bit is resilience,” says Paula DiPerna, who writes about the bond in her book. “So how do you value that? It’s tricky but you can quantify it if you look at the benefits.”

To do this, she explains, Blue Forest identified individuals and organisations — from insurers to California’s wildlife service and the local hydropower company — that stood to gain from improved forest management.

Benefits would show up in everything from lower insurance payouts to more funding for fire prevention and stable groundwater supplies for the hydropower company.

Beneficiaries pay back the funds over time with a premium. The bond, says DiPerna, sets out the benefits, quantifies them and then “secures investment upfront to securitise those benefits”.

Launched in 2018, the bond is currently repaying investors at contracted rates and has enabled forest restoration projects to be completed in four years, instead of the projected 10 to 12 years. Blue Forest is now developing a portfolio of similar forest projects.

The nature of nature

How do you measure and manage a resource that — as is the case for insects and fish, and for rivers and oceans — is constantly on the move? Given the sheer complexity of life on earth, there are no easy answers.

Moreover, nature’s economic value and relative health varies regionally. “None of this is universal,” says Goolgasian. “Everything is location-based. An acre of land in Brazil has a very different value from an acre of land in California or Congo.”

Even more challenging is the fact that much of nature consists of invisible forms of life that are not well understood. Katie Critchlow, former chief executive of NatureMetrics — which provides a biodiversity monitoring and reporting service based on eDNA (collected from a variety of environmental samples) — points to everything from genetic diversity within species to the beneficial bacteria that populate our guts.

“We’re starting to understand the importance of a world that we know very little about,” she says. This makes measuring carbon emissions, with a single key metric — a tonne of carbon dioxide — look simple.

And while carbon can be traded globally, nature cannot, says Thomas Crowther, a professor of ecology at ETH Zurich who studies the connections between biodiversity and climate change. “You can’t destroy a tropical forest in Brazil and plant some trees in Scotland,” he says. “With climate change, you suck a ton of carbon out anywhere on the planet and it has a global benefit.”

“It’s a very different case with nature,” agrees Leslie Cordes, who oversees the climate and energy, water, and food and forest teams at Ceres, a sustainable investing network. “Investors are also facing challenges in assessing the nature-related risk in their portfolios because it is so localised.”

One headache for investors is that the restoration of natural ecosystems does not happen overnight. “You have conservation projects that are all about biodiversity but that require an investment period and a time horizon that’s challenging for investors,” says Maria Teresa Zappia, global head of impact at asset manager Schroders.

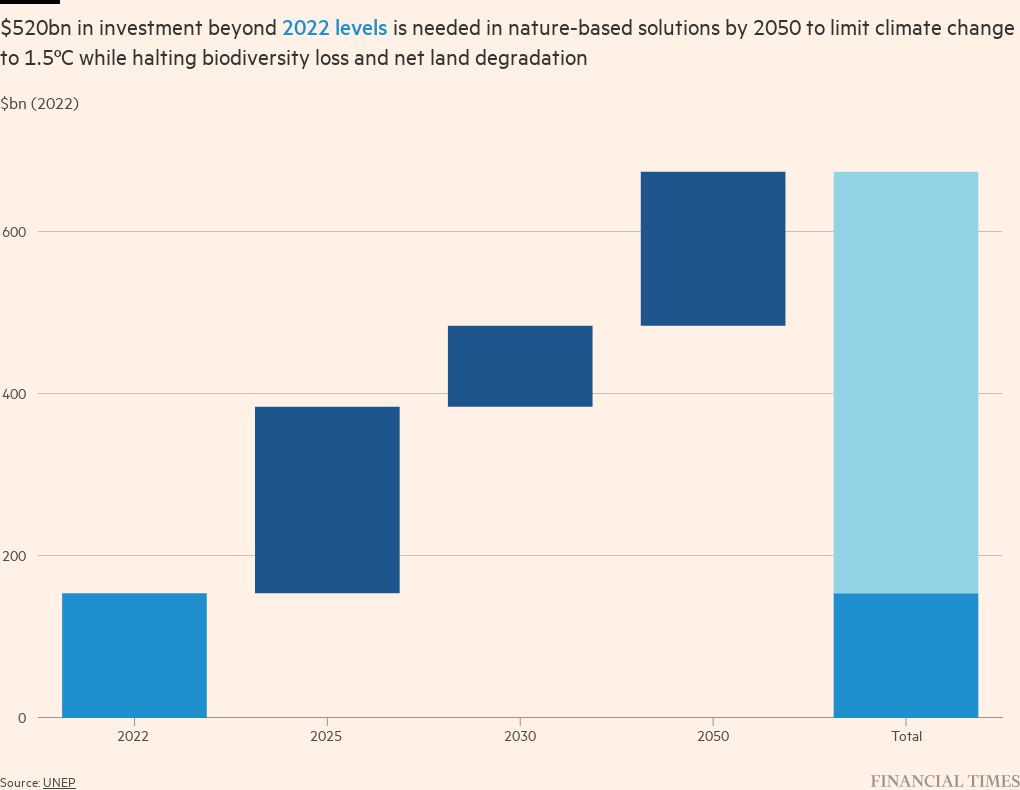

In 2020, the Financing Nature report estimated that shifting from conventional to sustainable agriculture practices on croplands can take up to seven years. Support needed while yields and farmer incomes adjust could total up to $420bn a year globally by 2030, according to the Paulson Institute, The Nature Conservancy and the Cornell Atkinson Center for Sustainability, which produced the report.

Still, private-sector executives may be energised by a growing realisation that nature and biodiversity are tightly linked to two other more familiar sustainability issues: climate change and water scarcity.

“Water is a key driver in nature and biodiversity loss so if we don’t think about water, we’re not going to succeed in protecting nature and building biodiversity,” says Kirsten James, senior director of the water team at Ceres.

Meanwhile, given the power of natural resources such as soils and forests to act as carbon sinks, companies with ambitious climate goals should have powerful incentives to invest in the protection of those resources.

Still, there is a danger that companies could use nature’s complexity as an excuse for inaction. Andrew Deutz, managing director for global policy and conservation finance at The Nature Conservancy, has heard this argument before.

“Some companies get it,” he says. “But I’ve had conversations with colleagues in the private sector who say, ‘Look, we’re just getting our head around climate, and that’s an existential threat — we don’t have the bandwidth to get our heads around nature’.”

Deutz’s response? “You have to deal with both.”

‘No data’ is no excuse

In a 2021 survey of investors by Credit Suisse, 70 per cent of respondents said that a lack of data was the key barrier to making investments supporting biodiversity. Two years on, the data landscape has transformed. New reporting frameworks are emerging and technologies such as satellite imaging and remote sensing are generating unprecedented amounts of information on the state of the world’s ecosystems and natural resources.

This does not make accounting for nature and biodiversity easy. In fact, companies and investors may well run up against nature’s version of the acronym-heavy “alphabet soup” that has characterised measurement and reporting standards in the environmental, social and governance space. And while the TNFD’s recommendations for corporate nature reporting have made an impact, they have not received universal acceptance.

With members from 40 large corporations and financial institutions, and with millions of dollars in funding from the Australian, Dutch, French, German, Norwegian, Swiss and UK governments, the TNFD has developed a global framework that can be used to measure, manage and disclose nature-related risks.

And as with the TCFD, governments may start requiring companies to file disclosures using the TNFD framework.

This worries some. In May, non-profit groups including the Rainforest Action Network, Global Witness and Greenpeace signed a letter to the TNFD’s co-chairs setting out criticisms of the recommendations for, among other things, insufficient emphasis on both human rights and supply chain transparency. They also highlighted the fact that the TNFD’s membership was dominated by executives from major corporations.

Goldner says that TNFD has since engaged with the non-profit groups through webinars. “They made a number of valuable written submissions which informed our thinking,” he says. “Many of their suggestions were incorporated into the final recommendations and accompanying guidance.”

Debates over the best way to account for nature will no doubt continue. And the TNFD is not alone in coming up with frameworks. For example, the UK’s Lancaster University has produced a Navigation Guide on Reporting on Nature to highlight best practice, while WWF (a TNFD partner) has produced a guide to help businesses identify and address biodiversity risks.

“There’s definitely an arms race in frameworks and standards,” says Wellington’s Goolgasian. “For an asset owner and management it can be difficult to determine what to prioritise to stay on top of all this.”

Nevertheless, he says, companies and investors can take some comfort from the fact that the TNFD based its framework on the TCFD, with which many in business and finance are now familiar. “This fits within existing systems. That’s very important.”

Meanwhile, technology is providing extraordinary new insights into what is happening on the ground, in the air and in the world’s water bodies.

Some systems supercharge ancient human practices. For example, a software tool called CyberTracker equips Bushmen in Africa, known for their animal tracking skills, with mobile devices that allow them to capture digitally the observations they collect on animal movements and combine that with data from satellite navigation systems.

And with more than 200 satellites, the fleet of Planet Labs, a US earth observation company, orbits the earth every 90 minutes, capturing its entire landmass daily. “We’re way past the date where we needed more technology to be able to assess things at a large spatial scale,” says Crowther, the ecologist.

Among the technologies emerging, he sees promise in bioacoustics, which involves planting microphones planted in ecosystems to monitor animals and birds. “You can hear the soundscape of the ecosystem,” he says. “And while you can’t tell every species that’s in there, you can still tell how that soundscape is more or less complicated compared to a natural soundscape.”

Crowther and his team are working on research that, using bioacoustics, is showing the positive results of Costa Rica’s decades-long programme of using a carbon tax to pay forest owners for ecosystem services. “The country has moved towards a more complex mix of high- and low-frequency sounds that reflect the recovery of life,” he says.

The ability to track levels of biodiversity accurately, and compare the relative success of different restoration treatments, makes it harder for companies to claim “lack of data” as a justification for not addressing their nature and biodiversity impacts and dependencies.

“That is starting to be challenged,” says Tamsin Ballard, chief initiatives officer at the UN Principles for Responsible Investment. “Yes, there’s different levels of granularity in different geographies, sectors and ecosystems, but there’s enough to get going.”

One step at a time

When we asked FT Moral Money readers whether their organisation had a biodiversity strategy with time-based targets, the largest group replied “No”. Getting going is not easy, it appears.

For companies that feel overwhelmed by the complexity of addressing their nature and biodiversity footprint, Walmart’s Kathleen McLaughlin has some advice. “Approach this first by understanding the most relevant concentrations of nature in your particular business, rather than trying to measure the nature impact of every single thing you do,” says McLaughlin, the retail chain’s chief sustainability officer.

Walmart is following this course of action. The US retailer started by working with non-profit group Conservation International on some calculations. “We worked out that very roughly it takes about 50mn acres of land and 1mn square miles of ocean to produce products our customers buy from us,” she says.

If this sounds daunting, McLaughlin says these kinds of calculations can be a starting point to help companies take practical steps to manage, conserve or restore nature and biodiversity. “For example,” she says, “the acreage analysis helped us identify the relative importance of engaging suppliers to adopt more regenerative agriculture practices in commodities such as row crops.”

The next step involves a process with which companies and investors are now familiar: determining materiality. A mining company, for example, could assess how its operations directly impact areas of high biodiversity value, while a computer manufacturer might track its sources of raw materials, how it uses those materials in its products, and how those products are consumed and recycled.

“It’s looking along the whole value chain,” says Samantha Deacon, principal for ecosystems solutions at Ramboll, an engineering consultancy. “And it will be different for companies in different sectors as to where they are in that value chain and the scale of their impact or dependency.”

But if companies feel unprepared for the challenge of managing their nature and biodiversity footprints, a growing number of tools are being developed to help them.

In fact, these tools are emerging so rapidly that the World Business Council for Sustainable Development has produced Eco4Biz, an overview of the existing tools that is designed to help companies decide which to use. BSR, a corporate social responsibility consultancy, also reviews and reports on new tools for measuring corporate impact on ecosystems.

Moreover, lessons learned from other types of sustainability strategies can be applied to nature and biodiversity. Walmart’s McLaughlin sees the “circular economy” approach as being especially relevant. “It’s a shift from an extractive mindset to one that’s about restoration, renewal, replenishment and resilience,” she says. “Essentially it’s regenerating the resources that get put to use.”

And while nature and biodiversity present different challenges, companies and investors can build on the sustainability strategies they have already developed.

This is the case for Nature Action 100, a new investor coalition following the model used by Climate Action 100+, which broke new ground by pushing companies to tackle climate-related risks.

Members of Nature Action 100, which is co-led by Ceres, are engaging around nature and biodiversity risks with 100 companies in sectors such as pharmaceuticals, chemicals, consumer goods, food, pulp and paper, and metals and mining.

Work done on climate change is paying off in other ways. Zadek at NatureFinance notes that the TNFD developed its framework in 18 months, compared with several years for the TCFD. “All that innovation and learning from the climate change agenda means we’re moving much more quickly to internalise nature-related analysis into financial institutions, central banks and financial regulators,” he says.

For companies, resources developed to tackle other sustainability challenges can be used to manage nature and biodiversity dependencies and impacts. This is true for Nestlé, which has a team of about 700 agronomists who work closely with farmers in its supply chain. “We’ll expand that existing resource so that it covers more than the traditional topics,” says Bethell.

He also stresses the need to connect climate and nature when it comes to developing in-house leadership. “Rather than having a biodiversity tsar, the approach at Nestlé is to integrate climate and nature,” he says.

This is critical, stresses Zadek. “You can’t sequence climate and nature — it’s not, ‘We’ve done climate so now we should get on with nature’,” he says. “The science tells us that these two things are completely interrelated.”

But Critchlow, the former NatureMetrics chief executive, warns of the dangers of replicating one mechanism used to tackle climate change: carbon credits. While she likes the idea of biodiversity credits generating finance for the restoration of nature, Critchlow worries they could come with the same credibility problems that have dogged carbon markets. “We need much better governance before everyone races ahead,” she says.

Nature’s complexity and regional variation mean biodiversity credit markets cannot operate in the same way as their carbon equivalents, she adds. “There’s no one fundamental price for nature as there is for carbon,” Critchlow says. “And you can’t kill a hippo in one place and save a rhino in another.”

Eyes on nature’s prize

When companies first started tackling their carbon emissions, they found some quick and easy wins. Energy efficiency initiatives, for example, had an immediate effect on the bottom line in the form of lower fuel bills. Such rapid returns on investment are harder to find when addressing nature and biodiversity.

But if the risks and opportunities presented seem less tangible, Ramboll’s Deacon points to a compelling reason for companies to start paying attention to nature. “You’re making your business more resilient for the future,” she says.

Bound up in this resilience are benefits that range from reduced risk of legal challenges, enhanced ability to attract ESG-focused investors and environmentally conscious consumers and employees, greater price stability of raw materials, and the ability to get ahead of future regulation.

Some FT Moral Money readers are convinced of these benefits. “Any company creating and implementing a biodiversity strategy will be safeguarding the ecosystem services on which it depends,” one wrote.

Another noted that rising concern about biodiversity will come with “new investment opportunities, in companies seeking to stop biodiversity loss”.

Financial innovation is also opening new avenues for investors. Ecuador’s debt-for-nature swap, for example, gives the country lower repayment rates on a $656mn loan, on the condition it uses some of the savings to fund environmental conservation. Investors include Legal & General, the UK’s largest asset manager, which purchased $250mn of the debt deal.

“Financial innovation is really important, and some of that is about new instruments like nature-linked sovereign debt and debt-for-nature swaps,” says Zadek. “That’s a rapidly emerging space.”

But perhaps the most powerful argument for taking nature and biodiversity seriously is an existential one, says Deacon. “You want to avoid diminishing natural resources till they run out,” she says. “Then you cease to be able to function as a business.”

Comments