The data is in: how QT impacts markets

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is professor of global economics at the MIT-Sloan School of Management, former external member of the Bank of England’s monetary policy committee and member of the White House Council of Economic Advisers

The Federal Reserve will discuss later this month whether to adjust its quantitative tightening programme that is unwinding the huge asset purchase operations it carried out to support the US economy and markets.

At least this will be a more informed discussion than when the central bank launched this QT programme in early 2022 and Fed chair Jay Powell warned: “I would just stress how uncertain the effect is of shrinking the balance sheet . . . ”

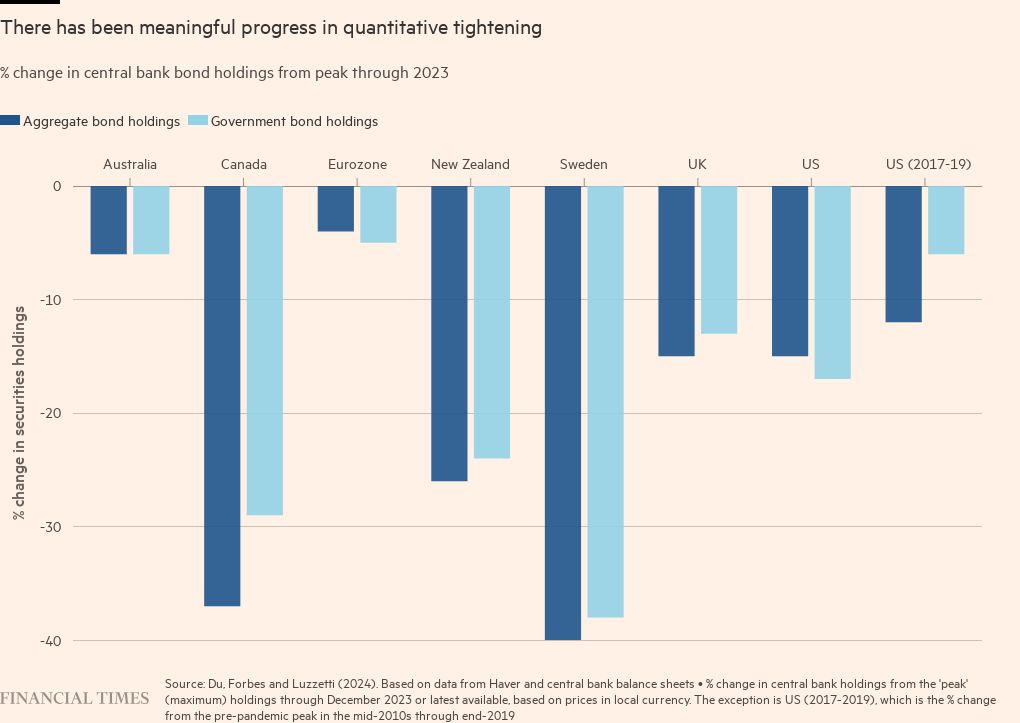

We finally have some international evidence on how QT works. Since the pandemic, seven central banks have made meaningful progress shrinking their balance sheets, in addition to the Fed’s QT from 2017-2019. A new study by myself with Wenxin Du and Matthew Luzzetti uses these experiences to assess the impact of announcing and implementing QT — as well as the advantages and disadvantages of different strategies.

QT programmes have, so far, been working as central banks intended. They are “in the background” and not seen as an active tool for adjusting monetary policy. At the same time, they have provided a small degree of support for central banks’ efforts to tighten financial conditions, with minimal impact on market functioning and liquidity. QT has worked in the opposite direction to quantitative easing, but the effects are much, much more muted.

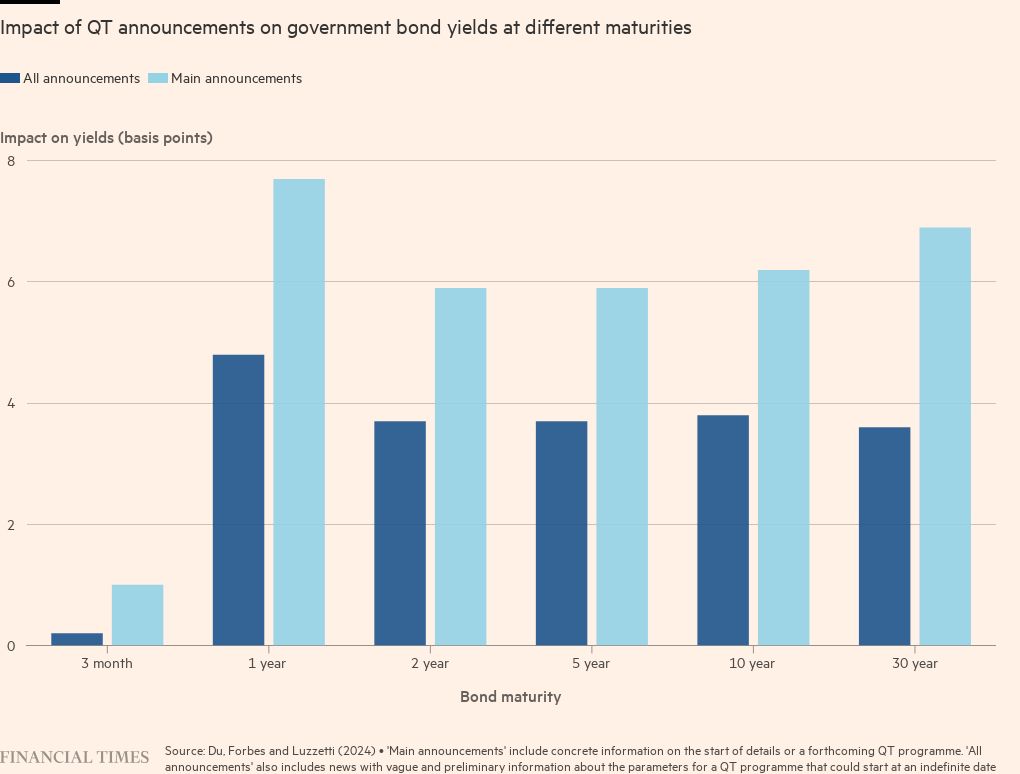

More specifically, announcing the start of QT causes a modest increase in yields (of about 0.04 to 0.08 percentage points) of government bonds with maturities a year and longer. Other effects are even harder to pin down — albeit generally pointing in the direction of tighter financial conditions. These muted effects continue when central banks begin implementing the programmes and some even selling their bonds outright. There has been minimal impact on bond pricing and liquidity, to date.

This is a big relief for central banks. Their large holdings of securities are generating political storms as higher interest rates translate into large losses that are passed on to Treasuries. Continuing to hold large parts of bond markets could raise difficult questions about the role of central banks.

Despite these concerns, central banks had been hesitant to start unwinding their holdings as they had little idea of the impact. A body of research suggests that QE had meaningful effects on financial markets — lowering interest rates, boosting equity prices and easing liquidity pressures. If QT had similar effects in reverse, the resulting tightening in financial conditions could undermine any recovery and keep policy interest rates stuck around zero. It was no wonder central banks were reluctant to start QT in the 2010s when growth was anaemic and inflation too low.

The rapid recovery and inflation spike in 2021, however, emboldened them to take the leap. Central banks in Australia, Canada, the euro area and the US announced passive QT — allowing bonds to roll off their balance sheets when they matured. Central banks in New Zealand, Sweden and the UK started active QT — outright bond sales. By the end of 2023, most had made substantial progress, with aggregate securities holdings down by about 40 per cent in Canada and Sweden, 25 per cent in New Zealand and 15 per cent in the US and UK.

So far, so good. We have also learnt about how different QT strategies work. Passive QT seems to provide a signal of the central bank’s commitment to tighter monetary policy, thereby increasing bond yields at the short end of the yield curve. Active QT mainly increases yields at longer maturities, steepening the curve.

One factor contributing to these relatively smooth adjustments so far is the willingness of “domestic nonbanks” to step in as central banks reduce their securities holdings. In the US, these incremental buyers include leveraged funds. Foreign investors have also been incremental buyers in some countries, but played a smaller role than expected in the US.

The path forward may be bumpier. Government debt issuance will be elevated for the foreseeable future, and the excess liquidity from emergency pandemic programmes has largely been absorbed. Nonetheless, now that we finally have some evidence on how QT works, central banks should be more comfortable shrinking their balance sheets in the future.

Comments