Too much Fed liquidity has led to a whack-a-mole world of problems

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is a philanthropist, investor and economist

The recent failure of Silicon Valley Bank combined two ingredients: excess deposits and losses on assets, even in securities such as Treasury bonds that are ordinarily considered “safe”.

SVB did not have adequate liquidity to tolerate a bank run and did not have adequate solvency to meet its liabilities. Emphatically, however, the failure did not occur because there was too little liquidity in the banking system as a whole. It occurred because there was too much.

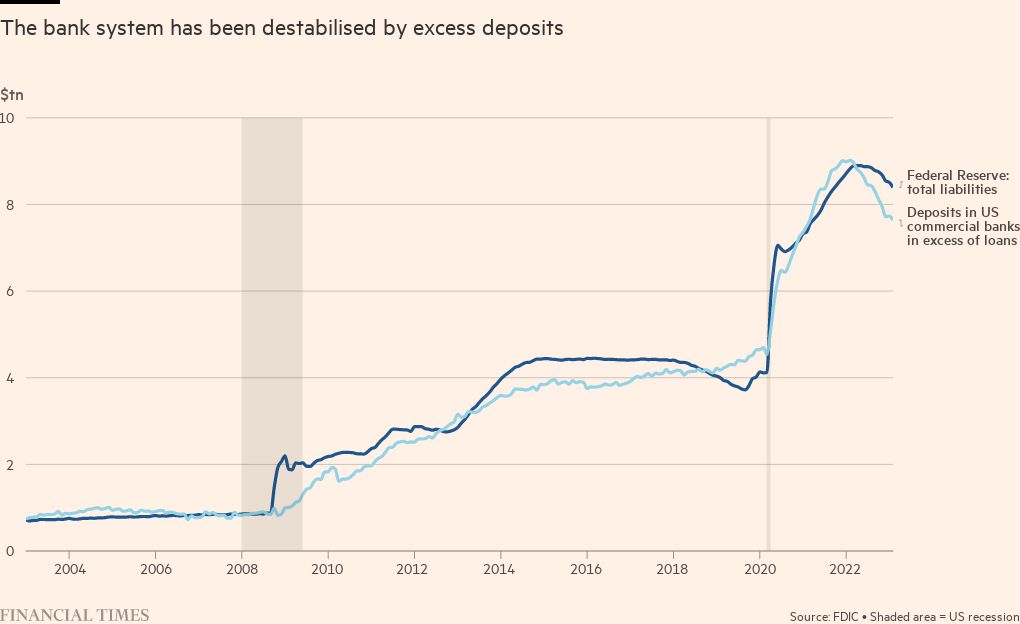

At the end of 2022, the US banking system had $18tn in domestic deposits, including an estimated $10tn of deposits insured by the Federal Deposit Insurance Corporation. That meant there were $8tn of deposits that exceeded the FDIC insurance limit.

Those destabilising excess deposits are there because in more than a decade of “quantitative easing”, the Federal Reserve took $8tn of bonds out of the hands of the public and replaced them with bank reserves.

Conceptually, one can think of a customer deposit as being “backed” either by reserves that the bank holds with the Fed or by assets such as an IOU that the bank received in return for a loan it made.

By buying trillions of dollars of bonds under quantitative easing, the Fed also in effect pushed trillions of dollars of deposits into the banking system, backed by newly created reserves rather than bank loans. Yet despite the most aggressive monetary expansion in history, the growth rate of US commercial bank loans (business, consumer, real estate) averaged just 3.4 per cent annually between 2008 and 2022, easily the slowest growth rate in data since 1947.

In 1852, Walter Bagehot wrote: “John Bull can stand many things, but he cannot stand 2 per cent.” For more than a decade, quantitative easing stretched that thesis to extremes.

Once the Fed created $8tn in base money, it ensured that, in equilibrium, someone in the economy would have to hold it indirectly as bank deposits, indirectly in money market funds or directly as physical currency.

All of the increased reserves — and associated bank deposits — earned nothing. Someone had to hold them, and nobody wanted to. The moment any holder attempted to put the money “into” a security, the seller of that security took the money right back “out.” Long-term securities, including Treasury bonds, were driven to record valuations because yield-starved investors, banks and pension funds could not tolerate the perpetual zero-interest rate world created by central banks.

Having engineered a toxic combination of excess bank deposits and yield-seeking speculation, the Fed ensured that instability would follow.

As I wrote in the Financial Times in January 2022, by relentlessly depriving investors of risk-free return, the Fed has spawned an all-asset speculative bubble that may now leave investors with little but return-free risk.

Investment losses have emerged since early 2022, both because inflation pressures forced the Fed to normalise rates after 13 years of zero-rate financial repression and because extreme valuations are never sustained indefinitely. The Fed can no longer operate monetary policy without explicitly paying interest to banks on the liquidity it created.

Sudden banking strains in the US and Europe, the British pension crisis last year, equity market losses — all these are merely symptoms of an unwinding bubble. The Fed itself would technically be insolvent if it was to mark its assets to market value.

In response to the insolvency of SVB, the FDIC took the bank into receivership, wiping out the stockholders and unsecured bondholders. This was, and remains, the proper approach to bank insolvency. The largest bank failure in US history — the 2008 failure of Washington Mutual — is unmemorable because it was also resolved in this manner. The FDIC took receivership. Stockholders and unsecured creditors lost because they were supposed to lose in this situation. Depositors lost nothing.

While the decision by the FDIC to cover uninsured deposits remains controversial, enhanced deposit insurance, funded by higher fees, may become necessary for a period of time. It is not the fault of savers that the banking system is drowning in excess deposits.

Savers, in aggregate, are captive victims of the Fed’s dogmatic “ample reserves regime”. Until it winds down this misguided experiment, global policymakers will continue their scramble to create new special programs, acronyms and emergency facilities to manage the whack-a-mole world of complications it has produced.

Comments