This is not a remake of 1999 for markets

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is chief investment officer at Julius Baer

With inflation decelerating and the American consumer remaining resilient, the bull market in US stocks is showing few signs of stalling even after the S&P 500 has risen 40 per cent from late 2022. Yet many investors are uneasy about the recent price action of the market leaders which have led this extraordinary rally, particularly the outperforming Magnificent Seven technology stocks.

It is true that from a technical point of view, the positioning of investors looks stretched and pockets of the US equity market are reaching overbought territory. However, observers making comparisons with the dotcom bubble are barking up the wrong tree.

First, it is important to look at the extremely generous liquidity injections that helped spur the dotcom market spike. The Federal Reserve was then easing monetary policy in response to the Asian crisis of 1997-1998. At the same time, European monetary authorities were cutting interest rates in preparation for the introduction of the common currency.

By comparison, in 2023, the market soared while the Fed continued its most aggressive tightening campaign in history, raising the federal funds rate by a cumulative 5.25 percentage points since March 2022. Furthermore, while liquidity in the system is still well above pre-pandemic levels, it is the change in the money supply that matters most for asset valuations. On a year-on-year basis, US M2 money supply is still contracting at a rate of 2.3 per cent. Today’s market cycle is not driven by loose monetary policy, in strict contrast to 1999.

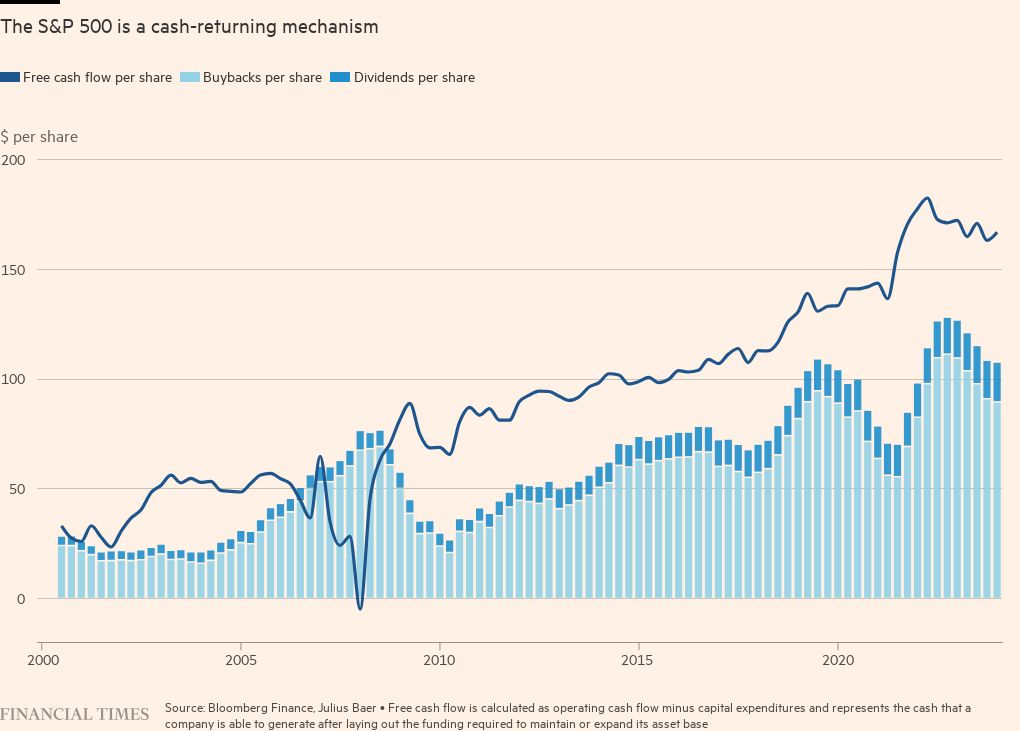

Second, today’s equity market rally has been underpinned by robust earnings and record production of free cash flow — cash generated from operations minus capital expenditures. This is particularly the case among the technology platforms, which are showing an extraordinary ability to convert a large portion of additional revenue into free cash flow.

Traditional valuation metrics, such as forward price-to-earnings ratios, show that the leading dotcom stocks were more than twice as expensive as today’s Magnificent Seven stocks. The story is similar on free cash flow yield — the amount of free cash flow generated per share as a percentage of the stock price. For the major tech names in the dotcom period, this was less than half that of today’s market leaders.

And US large-cap equities have morphed from a cash-raising to a cash-returning asset class. Apart from a secular decline in initial public offerings that is coupled with delistings, there is an increasing trend in share buy-backs. The best S&P 500 companies have become cash-returning machines.

Furthermore, there is currently no evidence of a bubble in price-to-earnings ratios. Investors who conclude that US large-cap equities are overvalued are implicitly discounting that free-cash-flow metrics, which have improved sharply in recent decades, will return to their long-term weaker mean.

Such a scenario is highly unlikely in the absence of a full-fledged reversal of globalisation and a reversal of US corporate tax rates back to 40 per cent. However, could there be a bubble in the earnings component, ie could earnings and their expectations be artificially inflated? Again, this is highly unlikely as companies are facing one of the most difficult liquidity environments in years. Furthermore, latest earnings calls point to relatively cautious corporate management behaviour, with a growing emphasis placed on capital deployment efficiency.

Third, US equities today are nowhere near as expensive relative to bonds as they were before the dotcom bubble burst. The forward-looking US real equity risk premium — the expected excess return that equities provide over benchmark bonds after adjusting for inflation expectations — stands close to its long-term median. Looking back at the same measure in 1999, equities were then priced in extremely expensive territory relative to bonds. The forward-looking US equity risk premium after taking into account inflation even turned briefly negative at the height of the internet frenzy. Moreover, the bond market is ramping up supply, with record volumes of issuance in the US corporate bond segment throughout January, while the US Treasury supply remains strong.

Overall, the stock market resilience in the face of normalised interest rates points to the outstanding quality of the current equity market returns. While an intermediate consolidation is likely, and even welcome to restore the market’s technical health, the secular bull market in equities is expected to continue. This is not a remake of 1999.

Comments