FTX: inside the crypto exchange that ‘accidentally’ lost $8bn

Simply sign up to the Cryptocurrencies myFT Digest -- delivered directly to your inbox.

It was all an $8bn accident. Or so says Sam Bankman-Fried.

As FTX, the crypto business led by the 30-year-old, quickly collapsed at the end of last week, many of its employees fled the Bahamas, the Caribbean country where the company was based. Some simply abandoned their cars at the airport.

Within the space of a few days, FTX had gone from being the vanguard of a new crypto economy, with a valuation of $32bn and celebrated by celebrities and politicians, to a humiliating bankruptcy.

As details of FTX’s finances and chaotic bookkeeping have been revealed this week by the FT and others, the focus of the investigations and legal battles is now on the gaps in the crypto exchange’s balance sheet — and especially $8bn of missing customer deposits.

The most innocent version of events that Bankman-Fried can present is that the missing customer funds were simply an oversight.

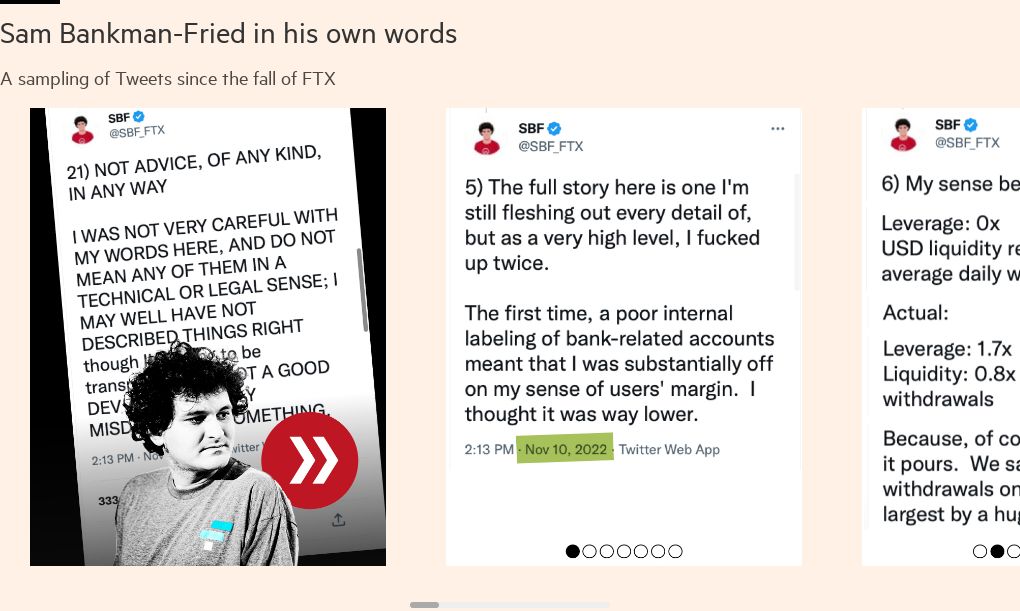

The MIT graduate, whose signature look combined unkempt hair and scruffy cargo shorts, acknowledged that FTX sent customer money to Alameda Research, the private trading firm he also controlled.

Bankman-Fried told the FT that the hole in FTX’s balance sheet was largely money shifted to Alameda, but that the move took place “accidentally”. (In a document shared with investors shortly before bankruptcy, the funds were listed as being in a “hidden, poorly internally labled ‘fiat@’ account”.)

In an interview with Vox, he described realising that the money intended for FTX had ended up at the trading firm: “oh fuck, people wired $8bn to Alameda and oh God we basically forgot”.

Many will find this explanation impossible to believe. As prosecutors, regulators, investors and up to 1mn creditors all ask questions about the missing funds, some are already convinced of a more nefarious version of events.

A class-action lawsuit filed on behalf of investors in the US on Wednesday alleged FTX was “truly a house of cards, a Ponzi scheme where [FTX] shuffled customer funds between their opaque affiliated entities”.

Interviews with close associates and seven former employees, including some who were at the company until its final days, portray an organisation that was chronically understaffed and which lacked basic security measures and financial controls.

The business was run more like a feudal court than a modern company, according to the employees. Decision-making and knowledge of the company’s affairs was restricted to Bankman-Fried and a handful of close friends in their late 20s, many of whom lived together in a luxury penthouse in the Bahamas. Loyalty was prioritised above all else.

The initial verdict from John Ray III, the veteran insolvency professional brought in to run the business, was devastating. “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here,” said Ray, who previously helped wind down Enron, the failed energy group.

As well as describing a company run by “a very small group of inexperienced, unsophisticated . . . individuals”, he highlighted potential illegality. The management failings at FTX included “the use of software to conceal the misuse of customer funds”, Ray wrote in the bankruptcy filing on Thursday.

Bankman-Fried has not responded to requests for comment for this article since last Saturday.

Most of the company’s employees had no idea the trouble it was in until it suddenly stopped paying out customer requests for withdrawals just days before its eventual collapse. Even staff who had worked for Bankman-Fried for years were left in shock.

“On the one hand, I am sad and panicking about what is going to happen next. But I am happy that this was exposed. I feel like there was so much toxicity in the company, from management, to the structure, to the company culture,” says one former employee.

“I think Sam was promoting loyalty over ability. I have seen so many companies walking towards death because the management is just the trust circle of whoever was in charge.”

Chaotic environment

Bankman-Fried’s fall has been so spectacular because more than anyone else, he had presented himself as the person who could take crypto mainstream.

His earnest, nerdy persona charmed figures from Wall Street regulators to the pop star Katy Perry.

Bankman-Fried’s fame was reinforced by lavish spending on advertising, from Super Bowl commercials starring Larry David to glossy Vogue magazine ads featuring supermodel Gisele Bündchen. Last year, FTX acquired the naming rights to the arena of the Miami Heat NBA team. He also donated heavily to the Democratic party.

The entrepreneur also wooed high-profile investors from BlackRock and Singapore’s state-owned fund Temasek to hedge fund Millennium Management’s Izzy Englander. He once mused about buying Goldman Sachs.

But even after accepting $1.8bn from outside investors, the company’s board consisted of just Bankman-Fried and FTX executive Jonathan Cheesman, until he stepped down in June. The single outside director was a lawyer from Antigua and Barbuda, where the company was incorporated.

Bankman-Fried based himself in an apartment in the 600-acre Albany gated compound in Nassau, famous as a location in the James Bond film Casino Royale and whose co-owners include Tiger Woods and Justin Timberlake. “Dubai is where people go to show off their money,” says one local resident. “Albany is where people go to keep it a secret.”

He shared a $40mn five-bedroom penthouse with the two other joint majority shareholders, head of engineering Nishad Singh and chief technology officer Gary Wang. At times, there were as many as nine housemates, including Alameda chief executive Caroline Ellison.

Both Singh and Wang were romantically involved with fellow staff, while Ellison and Bankman-Fried had been in an on-off relationship for roughly eight months, according to employees.

The romantic tangle prompted claims of favouritism. “A lot of people internally were not very happy with that management arrangement,” says a former employee. People outside the inner group, even in prominent positions, sometimes found out about key moves, such as acquisitions, on Twitter.

Singh, Wang and Ellison could not be reached for comment.

In theory, FTX and Alameda were separate entities to avoid conflicts of interest. But in reality, the exchange and the trading outfit were closely tied. A person who frequently visited the group’s Nassau offices said the Chinese wall was non-existent, with staff from the two companies sitting and working together in an environment they described as “mayhem”.

Bankman-Fried’s inner circle was knit together by longstanding personal ties, dating back to maths camp and MIT. But even some who share those bonds thought the penthouse clique was unhealthy.

“It’s like a dorm,” Sam Trabucco, former Alameda co-chief executive who stepped down in August, told the FT in April. “I think that’s toxic.”

Trabucco admitted, in an interview for FTX’s podcast, to working 134 days straight in late 2019 and early 2020, adding that he routinely worked 30-40 days without a break. He blamed his departure from the company on “burnout”, an experience shared by other employees.

Bankman-Fried was also notorious for working around the clock and snatching a few hours of sleep next to his desk. He tweeted about using substances to regulate his days. “Stimulants when you wake up, sleeping pills if you need them when you sleep,” he posted, in 2019.

Until the company’s rapid collapse, the chaos and extreme working routines could easily be cast as the hard-driving culture of an ultra-lean start-up.

No safeguards

That pared back structure, however, turned out to be one of the sources of FTX’s undoing.

Employees had raised red flags about security and safeguards at FTX before the crisis that engulfed the company.

Fewer than a dozen primary developers led by Bankman-Fried, Singh and Wang controlled the software and had full access to the company’s systems, the people said.

“I was always under the impression that the core code was restricted to the inner circle,” said a former employee.

The bankruptcy filings state Bankman-Fried and Wang “controlled access to digital assets” at FTX and used “an unsecured group email account . . . to access confidential private keys and critically sensitive data”.

Staff who had previous experience with similar companies were taken aback by the lack of normal checks and balances between functions such as development, security and product — teams that would normally monitor each other’s work.

“There was no corporate services team, no real general counsel team, no real back office, middle office, no clear CFO, all these were missing. There was really not enough structure,” says an executive at a company that worked closely with FTX.

Bankman-Fried resisted adding more staff or watering down the control he and top lieutenants exerted, former employees said. Senior figures in the crypto exchange urged the founder to staff up, share more responsibilities and reduce the company’s dependence on a few key developers.

“Sam [Bankman-Fried] told me he would rather take the risk of something blowing up than having someone who was not right for the culture,” says another former employee.

Bankruptcy filings state the company’s management used software to conceal the misuse of customer funds. The statement appears to support reports by Reuters that Bankman-Fried and close associates created a “backdoor” in the company’s accounting system that allowed vast transfers to cover losses at Alameda, while showing other employees and the outside world a healthy balance sheet.

Bankman-Fried denied the reports. He blames “messy accounting” for the leakage of funds to Alameda and for the failure to spot that his empire was far more leveraged and vulnerable to a bank run than he had recognised.

In a spreadsheet he personally prepared for investors during an eleventh-hour bid for funding to save the company, seen by the FT, Bankman-Fried wrote a confessional note: “There were many things I wish I could do differently than I did, but the largest are represented by these two things: the poorly labelled internal bank-related account and the size of customer withdrawals during a run on the bank.”

Final days

The FTX rank and file claim they were oblivious to the fact that the company was drifting towards disaster until early November. “Like everyone else, I had no idea that something had gone wrong with our financial situation,” a former employee said.

The crisis only became apparent to many on November 8, when FTX stopped processing client withdrawals. With no word from Bankman-Fried, developers confirmed to other staff that payouts had halted, and panic spread.

Hours later came news that Bankman-Fried and Binance chief Changpeng Zhao had agreed terms for the larger exchange to buy out FTX and backstop its liquidity problems. The deal to sell to an arch-rival had a devastating impact on the morale of FTX staff.

When the deal with Binance fell apart, Bankman-Fried resisted for several days, but after late-night talks with his lawyer and his father, he agreed to put the company into Chapter 11 bankruptcy around 4.30am on November 11.

But Bankman-Fried seems unable to admit defeat. In messages published by Vox, he insisted he was still trying to raise $8bn to pay back customers, but said he needed Wang or Singh to “come back”.

Both have abandoned the penthouse. Bankman-Fried said Wang is “scared” and Singh felt “ashamed and guilty” over losing customers’ money.

Much as Bankman-Fried appears not to have come to terms with his fall, employees were blindsided by the lightning-quick collapse, and the realisation that their former boss had betrayed both their trust and that of customers.

“We were the good guys . . . and it had come to this,” says one longtime employee. “We were once an empire.”

Additional reporting by Tabby Kinder, Antoine Gara, Dan McCrum and Scott Chipolina

This article has been amended after publication to correct the date on which Jonathan Cheesman stepped down from FTX’s board

Letter in response to this article:

What links FTX, James Bond and age of piracy? / From Paul Hallwood, Storrs, CT, US

Comments