Simplicity is key to avoiding a gap in investment returns

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Morningstar calls its annual funds study the Mind the Gap report, using the warning introduced on the London Underground in the 1960s. They could equally well have used a phrase popularised by the US Navy around the same time, namely: “Keep it simple, stupid.”

The study measures the returns generated by investors in US mutual funds and exchange traded funds (ETFs), and it’s as telling as any academic research in behavioural finance.

It consistently shows that investors’ returns are lower than the returns of the funds themselves, because of poorly timed purchases and sales of fund shares. It has an equally consistent message about what investors should be doing to narrow the gap.

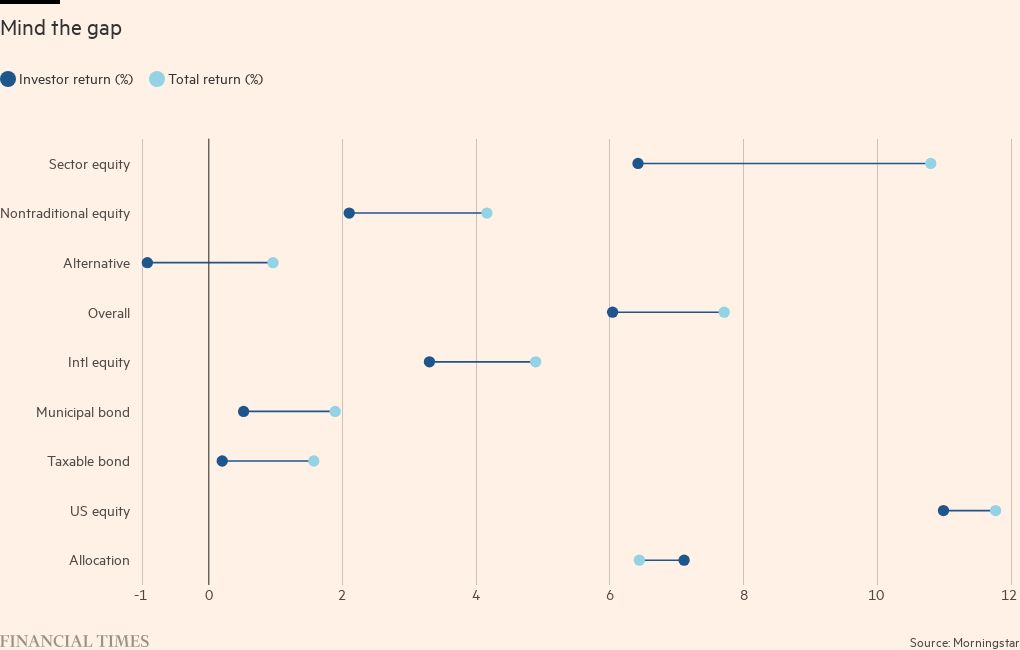

The latest study, based on data for the 10 years to the end of 2022, showed that the average dollar invested in ETFs and mutual funds returned 6.0 per cent per year. The funds themselves reported returns of 7.7 per cent. The gap of 1.7 percentage points means investors missed out on almost a quarter of the money they would have made if they had simply bought and held over the 10 years.

There’s an irony here: Morningstar is also the creator of the most-used star rating system for mutual funds and ETFs, which grades funds based on their historic performance and has arguably entrenched investors’ tendency to pile into investments after they have run up.

The key point of Mind the Gap is that investors too often buy high and sell low. Drill down, and it is instructive to see where the gap is widest and where it is the most narrow.

Investors fared best in what Morningstar calls “allocation funds”. These are vehicles that contain a mix of asset classes, such as target-date retirement funds designed as set-it-and-forget-it investments for the long term. The gap between fund returns and what investors took home was less than half a percentage point.

Jeffrey Ptak, chief ratings officer at Morningstar, and his colleague Amy Arnott wrote that this finding — consistent through the study’s history — shows how having multiple asset classes in one package, “lessens the need to maintain positions and, more prosocially, mitigates the risk that an investor will respond impulsively to the performance of any one component”.

Some of the most disappointing results were in categories that have been marketed heavily to wealthy investors, in funds that use hedge-fund-like strategies.

So-called non-traditional equity funds, which include long/short strategies or use derivatives, returned 2.1 percentage points less to the average investor over the decade, meaning investors captured barely half the fund managers’ underlying performance. In “alternatives” funds, which use asset classes beyond traditional stocks and bonds, the 1.9 percentage point gap wiped out all the funds’ underlying returns and then some.

Wealth managers may encourage their clients to build portfolios that mimic endowments and other long-term investors with these alternative strategies. Morningstar’s analysts caution that these are “more exotic strategies that, on paper, might push a portfolio closer to the efficient frontier but, in real life, confound investors into costly mistakes”.

The risks of following fashion or chasing hot fund managers are laid bare also in sector-based equity funds, where a 10.8 per cent annual return for the underlying funds translated into just a 6.4 per cent return for the average investor: a 4.4 percentage point gap.

These are among the most volatile categories of funds, and, while I wouldn’t be as rude as Warren Buffett in likening their fans’ behaviour to “an army of manic-depressive lemmings”, the figures do suggest it is hard to get the timing right on sectoral calls.

Earlier this year, the Financial Times highlighted the case of Cathie Wood’s ARK Disruptive Innovation ETF, which was emblematic of the mini tech bubble of the pandemic period. It pulled in $3bn in a crazy two-week period in February 2021, when the fund was up more than 700 per cent from its launch, taking its assets to a peak of $27.9bn.

By March 2023, when the FT reported figures from Morningstar and FactSet, the stock had fallen 74 per cent and the average dollar invested in the fund over its nine-year life had shrunk to 73 cents, evaporating $9.5bn of investor cash. Its share price has not improved since.

As an aside, the Mind the Gap study probably underestimates the size of the foregone returns in all the different categories because of the way Morningstar treats ETFs. It uses only month-end data, in order to be comparable to mutual funds, so it does not capture daily trading where speculators are likely to be making additional mistakes along the same costly lines.

One intriguing bright spot in the report: investors in active funds seem to be capturing more of the underlying returns than those using passive vehicles. Morningstar says that the unrelenting shift of money from active to passive means that a meaningful portion of passive funds’ asset base wasn’t around to participate in the returns of the full 10-year period, missing some of the more profitable stretches but catching last year’s bear market.

I think there might be another factor, too, namely: these are investors who have decided to pay an active manager to make decisions for them, and might be less likely to do it themselves by flitting from sector to sector, strategy to strategy and fund to fund. In a bear market, an active manager is there to talk you out of selling at the bottom.

Morningstar concludes with several lessons for investors, which apply to those with large or small sums in the market: “Hold fewer, more widely diversified funds”; “Avoid narrow or highly volatile funds”; and, above all, “Keep it simple”. That way, you really will “mind the gap”.

Stephen Foley is the FT’s US accounting editor. Follow Stephen on X @StephenFoley

This article is part of FT Wealth, a section providing in-depth coverage of philanthropy, entrepreneurs, family offices, as well as alternative and impact investment

Comments