The case for continued American equity exceptionalism

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is a former chief investment strategist at Bridgewater Associates

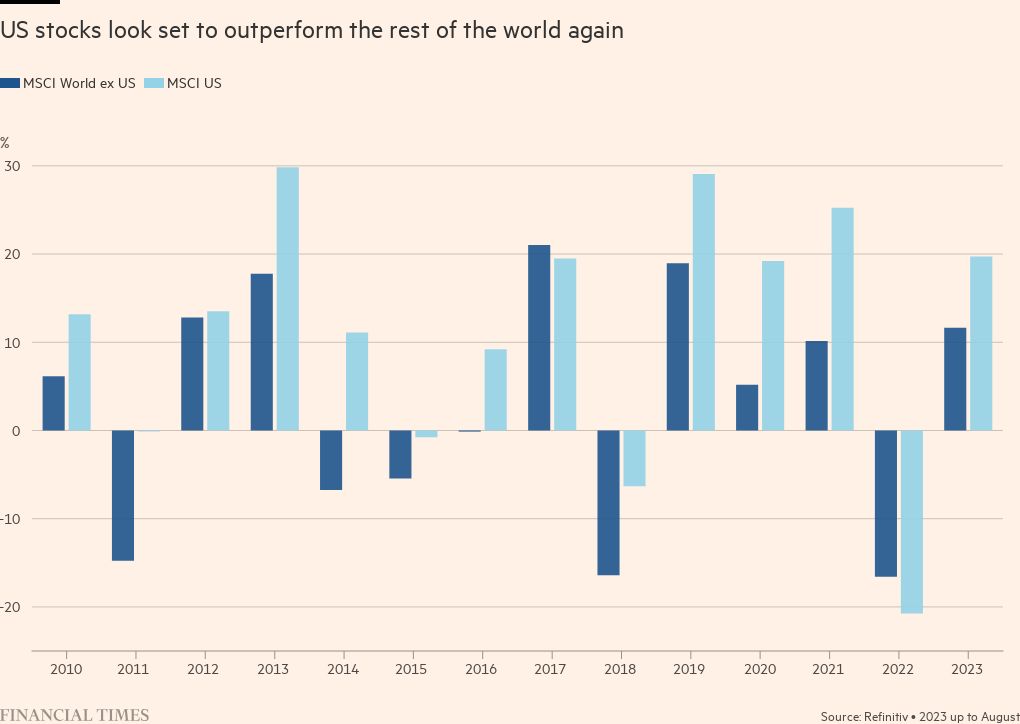

After outperforming peers for 12 out of the last 13 calendar years, could US equities dominate for another decade?

At first glance, another 10 years with the US on top seem unlikely. History shows relative equity performance alternating between US and non-US equities. High valuations, margins and ownership eventually all sow the seeds of a handoff, especially when there is a new growth catalyst. The popping of the US technology bubble in the early 2000s coupled with the growth emerging from China joining the World Trade Organization illustrates the dynamic: after years of US equity leadership in the 1990s, the baton was passed in the 2000s to more China-centric markets.

But a second look suggests more American equity exceptionalism is possible, for at least two reasons. First, the US is set to capture a sizeable share of productivity benefits from technology such as artificial intelligence. Second, a moderating global economy could work against more cyclically biased equity markets overseas, favouring those geared towards organic growth drivers. Diversification remains, as Nobel Prize winner Harry Markowitz famously said, “the only free lunch in finance”. But for global investors, economic prospects over the coming years suggest that meal might taste better with an abundant helping of US stocks.

This is not to write off diversification across asset classes and geography. Any investor hoping to increase long-term wealth through compounding returns will want to manage risk from idiosyncratic events. It also is not to suggest that over a shorter period – months or even quarters - the US won’t at times lag behind other markets, just as it did at the turn of this year as China reopened and Europe was less economically damaged than expected. But over the next decade, there is good reason why Markowitz’s principle may at least be geographically challenged.

First, over multi-year periods, domestic growth has been found to dominate local equity returns. A 2011 study by Clifford Asness, Roni Israelov and John Liew suggests that 39 per cent of 15-year returns could be explained by domestic economic performance. Growth is fundamentally a function of labour and productivity. Given that most of the developed world (and China) faces at least directionally similar labour constraints, the US seems likely to be a relative growth winner thanks to prospects for greater productivity gains.

Specifically, the gradual diffusion of technological advances through the economy, led by AI, could give a productivity boost to US growth. A recent report by Goldman Sachs estimated that widespread adoption of generative AI could raise overall US labour productivity growth by 1.5 percentage points a year, roughly doubling the recent pace - that’s in line with the effect of the personal computer. The report estimates that this force, all else being equal, could lift US gross domestic product growth by 1.1 percentage points for 10 years.

US tech dominance could benefit respective equities over the next decade in another way: the weight of technology in US equity benchmarks. Thanks partly to large overhangs of government debt, deteriorating demographic backdrops (more retirees and fewer workers) and more fragmented economies, we may well see a trend of moderating global economic growth. The IMF, in its April World Economic Outlook, noted that its five-year-ahead global GDP growth forecast had fallen from 4.6 per cent in 2011 to only 3 per cent.

Without significant cyclical momentum, companies with more structural, organic sources of growth are likely to capture an investor premium. US equity index benchmarks have notably smaller weightings of companies that depend on cyclical growth than peers do. Data from Morningstar Direct, for instance, shows non-US equity benchmarks have significantly more exposure to industrials and basic materials, while the US has more than double the weight on technology compared with peers.

This doesn’t rule out a near-term pull-back by US mega-cap tech stocks, or relatively stronger near-term equity performance in another country or region. But in thinking about longer-term portfolios and why equity leadership has shifted over the last several decades, it comes back to growth and what’s driving it. For now, it is difficult to see what could lead to a macro environment reminiscent of 1980s Japan or 2000s China and emerging markets.

A US economy that is relatively stronger than its peers, thanks in large part to a comparative advantage in key technologies along with growth that’s being driven less by cyclical forces than structural ones, suggests US equities are more likely to remain in the winner’s circle in the coming decade.

This article has been amended to correct an editing error on the title of Rebecca Patterson at Bridgewater

Comments