Pension shift will change the UK financial landscape

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Defined benefit pension assets are invested for one reason and one reason only: to solve a problem. This problem is how to meet (mostly historical) income-in-retirement promises made by employers to their staff.

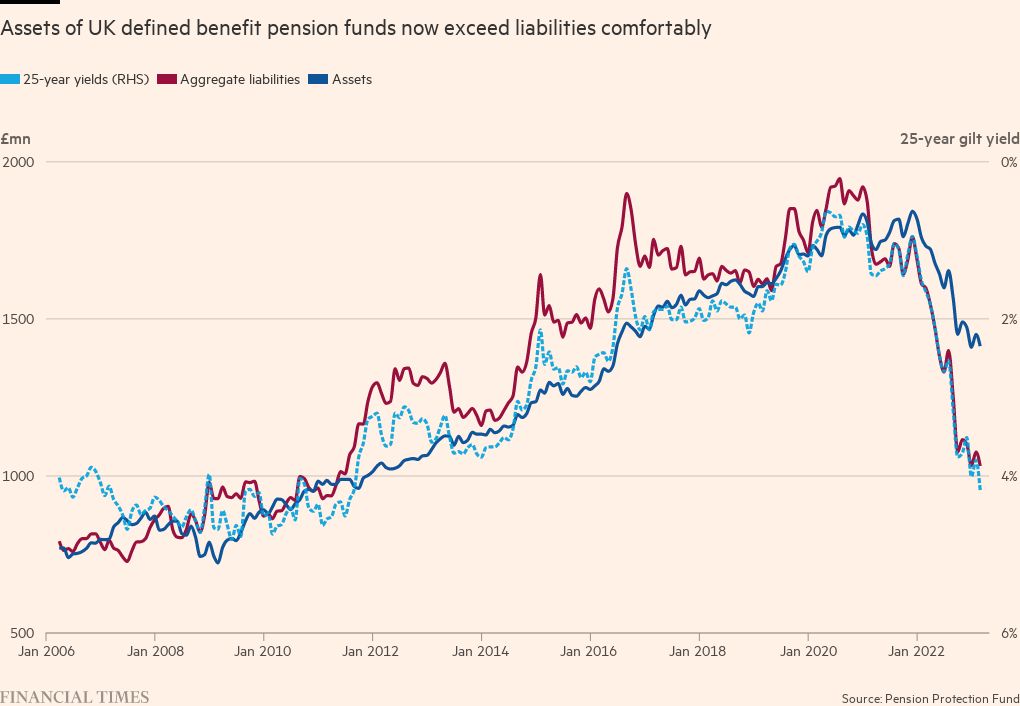

Pensions represent a greater portion of British household wealth than housing, and the UK is unusual in having so much of its pension promises fully funded. To put this in an international context, UK pension assets account for 120 per cent of UK GDP, far more than Germany (8 per cent), France (12 per cent), or Japan (31 per cent), although less than the US (174 per cent), according to the OECD. Funded defined benefit schemes hold about £2tn of assets, and defined contribution schemes account for a further £213bn.

Since the ONS began counting in 2004, private firms have made £520bn of employer cash contributions into the DB schemes they sponsor. While 2022 has hit asset values to the tune of £400bn, the monumental rise in bond yields has shrunk the present value of their liabilities by even more, leaving schemes in a vastly improved financial position. (When bond yields rise, the present value of pension liabilities falls.)

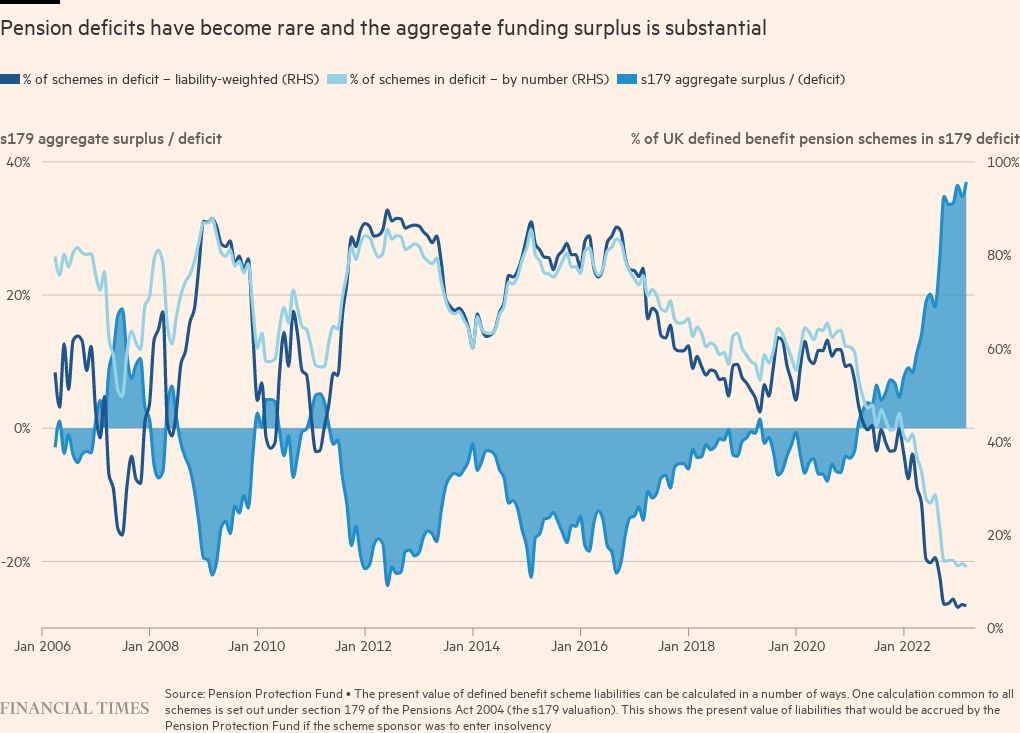

Such has been the combination of outsized employer contributions and rising bond yields, the problem that such schemes exist to address — how to provide pension security to retirees — has now largely been solved. For current and future retirees lucky enough to have access to a defined benefit pension this is wonderful news. So too is it for firms exhausted by their pension fund’s seemingly perpetual calls for fresh capital. But from a societal perspective, the disappearance of this problem throws up new challenges.

Firms sponsoring well-funded DB schemes can offload their obligations towards members, in what is known as the bulk annuity or “buy-out” market. This is the end goal of many sponsors. For a price, an insurance company will take over the responsibility for paying their retirees. This price is typically paid in cash and gilts, and the assets are then invested by the insurer into a range of bonds, private debt and equity release mortgages. According to LCP — an investment consultant that has advised on 35 per cent of large transactions since 2014 — about £340bn of pension assets had already transferred by the end of 2021, and record volumes are being anticipated as more schemes declare the job done.

The accelerating exit of the gilt market’s main participant has profound implications for fixed income market structure, government financing, the transmission of monetary policy, as well as aspirations from within government, the City, and beyond that our vast pension assets be deployed in a manner that funds growth and innovation. But it also ushers in a new investment landscape where a small group of insurers will have immense market power.

Today, the interests of the 10.1mn members of private sector DB schemes are overseen by about 5,200 boards of trustees, their advisers and their managers. The LDI crisis made plain that investment strategies lacked the kind of heterogeneity in risk exposures that might be assumed to flow from such a large population of investors. But a future in which eight insurers dominate the market does not seem entirely unproblematic either.

A number of asset management business models rely on there being a large stock of UK DB pension assets to manage and these models will change. But despite the accelerating run-off of DB pensions, most people I speak to in the industry are relatively relaxed.

One factor providing comfort is the illiquidity of well-funded schemes. It is hard to go into buy-out when a meaningful portion of your assets are stuck in frozen commercial property funds, or locked up in private equity vehicles. Illiquid assets are still valued regularly, but there is a strong suspicion that they might be “marked-to-make believe” following last year’s public asset market rout. And selling illiquids can only reasonably be done at very large discounts to their quoted values. Doing so would invite challenge to trustees in their roles as fiduciaries.

Secondly, there are major supply-chain bottlenecks that have built up at pensions administrators. Double-checking that correct spousal details are coded in the right systems for tens or hundreds of thousands of scheme members is slow work, and there is simply insufficient capacity to complete the paperwork demanded by insurers. As one consultant put it to me, the capacity to migrate to buy-out looks to be only £50bn a year which is little more than a rounding error in the context of a £2tn pensions market. The constraints are real. But they are not permanent. A world of change is coming to the UK’s financial landscape.

Comments